Buy Time Technoplast Ltd for the Target Rs.280 by Motilal Oswal Financial Services Ltd

Healthy in-line quarter; robust outlook intact

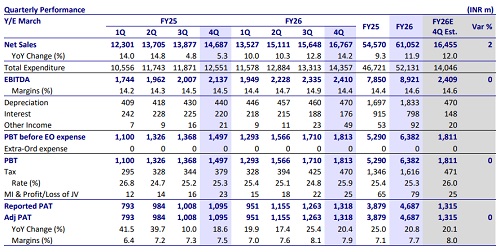

Revenue/EBITDA/PAT jumps 14%/13%/20% YoY in 4QFY26

* Time Technoplast (TIME) reported a healthy and in-line set of results in 4QFY26 despite ongoing geopolitical tensions in West Asia.

* Volume/revenue/EBITDA/PAT grew ~13%/14%/13%/20% YoY. EBITDA margin stood high at 14.4%, while PAT margin improved 41bp YoY to 7.9%. The Indian market led volume growth of 14.2% YoY (overseas up 11.4%).

* Value-added products (VAP) revenue grew 20% YoY with an 18.9% EBITDA margin. Established product revenue rose 12% YoY, with a 13.1% EBITDAM.

* For FY26, volume/revenue/EBITDA/PAT grew ~15%/12%/14%/21% YoY.

Key highlights from the management commentary

* Revenue growth guidance: Overall 15%+, Packaging Products 11-13%, Composite 25-30%, PE Pipes 20-25%

* Margin levers: efficiency improvement, manufacturing consolidation, manpower cost reduction on automation, adoption of solar solutions

* RoCE guidance fell a little short of 20% in FY26 due to QIP-led equity dilution; it aims for a 1.5–2.0% annual improvement.

* Focus remains on higher-margin VAP sales (up 20%/18% YoY in 4QFY26).

* Despite INR3.7b capex in FY26, debt reduced by INR4b aided by QIP money

* Extended due diligence review period to acquire an identified FIBC firm

* The acquisition of Systoverse Pvt. Ltd for ~INR250m is in the final stage.

* Use of solar power at a few plants reaped an annualized benefit of INR110m; more savings are likely from 3QFY27 as other plants implement it.

* In the process of obtaining approvals for 250 and 350-liter CNG cascades.

* The launch of 14.2 kg LPG cylinders is delayed due to the shortage of gas.

* Engaging with suppliers to bring fire extinguisher products to market; the initial target segment is oil refineries, providing ~0.8m units of annual demand.

* Plant consolidation of CNG composite cylinders and capex were completed to take capacity from 480 to 1,080 cascades.

* The recycling 1st plant of 12,000t capacity is operational at Bhilad (Gujarat).

* The IBC cage line brownfield expansion of 150k unit capacity is completed; phase-2 of 150k unit capacity is expected by FY27-end.

* It is expanding the Georgia, US facility to add an IBC line along with a drum manufacturing line to further strengthen its presence in the region.

Valuation and view: reiterate BUY

* We maintain our earnings estimates following an in-line result in 4QFY26.

* After clocking a 15%/18%/35% CAGR in revenue/EBITDA/PAT over FY21-26, we estimate a 15%/16%/21% CAGR over FY26-28, led by the VAP segment.

* Despite a QIP-led equity dilution, pre-tax RoCE/RoIC are expected to expand to ~19%/22% in FY28 (FY24: 16-17%), driven by healthy operating results, improved efficiency, and working capital management.

* The robust outlook and attractive valuation (~12.5x FY28E P/E) warrant a rerating, in our view. Reiterate BUY with a TP of INR280 (20x FY28E P/E).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041