Buy Tech Mahindra Ltd For Target Rs. 1,900 by Motilal Oswal Financial Services Ltd

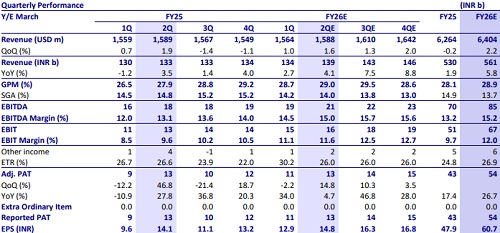

* We expect revenue to grow 1.0% QoQ CC, largely driven by ramp-ups of recently won deals. We believe Hi-Tech remains muted due to weakness at a semiconductor client, though some stability is visible this quarter.

* BFSI and Retail should drive growth. Manufacturing (dragged by US Auto) and Communications are likely to remain flat with early signs of stabilization. Management sees a sustainable TCV baseline of USD600-800m.

* EBIT margin expected to improve by 50bp QoQ to 11.6%, supported by lower subcontractor costs and SG&A efficiency. We build in 13% exit margin by FY26.

* The outlook on margin gains and segments such as BFS vertical and CME, especially in US and deal TCV, will be the key monitorable.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412