Buy Tata Consultancy Services Limited for Target Rs. 3255 - Religare Broking Ltd

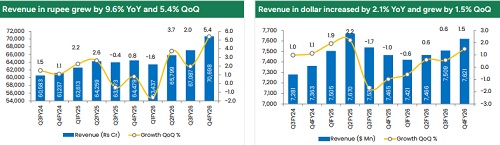

Strong Financial Performance & Margin Expansion: TCS delivered a solid Q4 FY26 performance, with revenue at ?70,698 crore, reflecting steady growth despite global uncertainties. Net profit rose 12.2% YoY to ?13,784 crore, supported by operational efficiencies and better cost control. A key highlight was operating margin expansion to 25.3%, a four-year high, driven by improved utilization, pyramid optimization, and higher realization from premium services. For the full year, margins remained strong at 25%, showcasing consistency. Despite currency headwinds in dollar terms, the company maintained profitability through disciplined execution, indicating resilience in a volatile macro environment.

AI-Led Transformation Driving Growth: A major structural shift is TCS’s rapid transition toward AI-led services. Annualized AI revenue crossed $2.3 billion, signaling a move from pilot projects to enterprise-scale deployment. The company’s “infrastructure to intelligence” strategy positions it as a full-stack AI provider, covering cloud, data, and AI solutions. Strategic partnerships with players like OpenAI and AMD are strengthening capabilities. Importantly, clients are shifting toward outcome-based pricing, improving realizations and margins. AI is now becoming a core revenue driver rather than an experimental segment, supporting long-term growth visibility.

Robust Deal Wins & Order Book Visibility: TCS reported strong deal momentum with a Q4 Total Contract Value (TCV) of $12 billion, including multiple mega deals. This contributed to a robust full-year order book of $40.7 billion, providing strong revenue visibility ahead. The company also demonstrated strong client engagement, with growth across large client buckets, including the addition of new $100M+ and $50M+ clients. This indicates deeper relationships and higher wallet share from existing customers. The strong pipeline reflects sustained demand for digital transformation and AI-led solutions, positioning TCS well to navigate macro uncertainties and maintain steady growth momentum.

Demand Trends & Segment Performance: Demand trends remained mixed across geographies and verticals. Energy, Resources & Utilities and Consumer segments led growth, while BFSI- TCS’s largest vertical remained subdued due to cautious spending globally. Regionally, the UK was the strongest performer, while North America showed gradual recovery. However, some regions like Asia Pacific and emerging markets faced pressure due to weaker discretionary spending. This divergence highlights a selective recovery environment, where clients are prioritizing cost optimization and efficiency-driven projects over discretionary IT spending, thereby favoring AI, cloud, and automation-related investments.

Workforce Strategy & Operational Efficiency: TCS ended FY26 with a workforce of 584,519 employees, reflecting a focus on productivity and efficiency. The company announced salary hikes effective April 2026, including double-digit increases for top performers, signaling confidence in future demand. A key strategic focus has been large-scale upskilling, with over 270,000 employees trained in AI and machine learning. This investment ensures readiness for the next technology cycle. Margin expansion was supported by better utilization, pyramid restructuring, and automation. The company’s ability to deliver growth with a leaner workforce highlights its transition toward a more efficient, AI-integrated operating model.

Outlook & Valuation Perspective: Tata Consultancy Services management remains optimistic for FY27, supported by a strong deal pipeline, rising AI adoption, and sustained client investments in technology. While geopolitical and macro uncertainties persist, AI-led services are expected to be net accretive to growth over time. The company continues to command a premium valuation, backed by strong margins, consistent cash flows, and leadership in digital transformation. Its transition toward an AI-driven, platform-led model enhances long-term earnings visibility. We estimate Revenue/EBIT/PAT CAGR of 5.6%/3.5%/3.2% over FY26-28E and maintain a BUY rating with a target price of ?3,255

Key Highlights:

* Future Growth Driven by AI & Digital Transformation: Tata Consultancy Services’s future growth is increasingly anchored in AI, cloud, and digital transformation. With AI revenue already crossing $2.3 billion (annualized), the company is transitioning from experimentation to enterprise-scale deployments. Strong deal wins and a $40.7 billion order book provide multiyear revenue visibility. Clients are prioritizing cost optimization and automation, where TCS is well positioned. The company’s “infrastructure to intelligence” strategy and partnerships with global AI leaders strengthen its competitive moat. Over the medium term, AI-led services are expected to become a key growth engine, offsetting slower growth in traditional IT outsourcing segments

* IT Sector Growth Outlook & Industry Trends: The Indian IT sector has crossed the $300 billion mark and continues to grow, though at a moderated pace amid global uncertainties. Growth is expected to remain in the mid-single digits in the near term, with gradual acceleration driven by AI adoption, cloud migration, and digital engineering. However, the FY27 outlook remains cautious due to geopolitical risks and weak discretionary spending in key markets like the US and Europe. The sector is undergoing a structural shift from labor arbitrage to technologyled transformation, where value creation will depend on innovation, platforms, and domain expertise rather than scale alone.

* Key Tailwinds Supporting the Sector & TCS: Several structural tailwinds support TCS’s long-term growth. Rising enterprise AI adoption is creating new demand pools, especially in automation, analytics, and cybersecurity. Large enterprises are accelerating digital transformation, ensuring sustained deal pipelines. Currency depreciation also benefits exportoriented IT companies by boosting margins. Additionally, BFSI, energy, and manufacturing sectors are resuming tech spending, providing demand stability. India’s strong talent base and cost advantage continue to attract global outsourcing deals. These factors collectively position TCS to maintain steady growth, even in a volatile macro environment, while capturing emerging high-value opportunities in AI-led transformation

* Headwinds & Structural Challenges in the IT Sector: Despite strong tailwinds, the sector faces meaningful headwinds. Global macro uncertainty, geopolitical tensions, and cautious discretionary spending continue to impact demand visibility. AI itself poses a structural risk by automating repetitive tasks - the core of traditional IT services. This could compress pricing and reduce volume growth in legacy services. Additionally, verticals like BFSI and retail remain cautious, delaying large-scale tech investments. Margin pressure may also arise from wage inflation and continued investments in AI capabilities. As a result, IT companies must continuously evolve their business models to sustain growth in an increasingly competitive and technology-driven landscape

* Shift from Services to a Platform-Led, Subscription-Based Model: TCS is gradually transitioning from a traditional time-and-material services model to a platform-led, outcomebased, and subscription-driven business. Clients are increasingly opting for managed services, cloud platforms, and AI-driven solutions with recurring revenue models. Products like TCS ignio™, AI platforms, and cloud-based offerings are enabling this shift. Outcome-based pricing improves revenue predictability and margins while reducing dependence on headcount growth. This transition marks a structural evolution in the IT industry from linear growth tied to employee addition to scalable, IP-led growth driven by platforms and recurring revenue streams.

* AI Products, Growth Visibility & Valuation Perspective: Tata Consultancy Services is building a strong AI ecosystem through platforms like ignio™, HyperVault (AI infrastructure), and partnerships with OpenAI and AMD. With over 270,000 employees trained in AI, it has one of the largest AI-ready workforces globally. AI is expected to be net accretive to revenue growth, supporting long-term visibility. From a valuation standpoint, TCS commands a premium due to consistent margins, strong cash flows, and leadership in digital transformation. While near-term growth may remain moderate, its structural shift toward AI-led platforms continues to support growth visibility.

Please refer disclaimer at https://www.religareonline.com/disclaimer

SEBI Registration number is INZ00017433