Buy Star Cement Ltd for the Target Rs.280 By Emkay Global Financial Services Ltd

We interacted with the senior management of Star Cement (Star), for a deep dive into their growth plans and competitive scenario in the Northeast. KTAs: 1) Explicit plans of reaching clinker-backed installed capacity of ~18mtpa (vs ~8mtpa now) by FY29/30. 2) The upcoming 2mtpa GU in Begusarai, Bihar will aid Star in not just serving the high-yielding markets of central and western Bihar, but also enjoying 300% SGST benefits. 3) The upcoming railway line from Lanka (Hojai district, Assam) to Umrangso (Dima Hasao district, Assam; news link) will reduce logistics cost (per ton per km) by ~33%, along with helping transport clinker from the upcoming clinker line in Umrangso to its Bihar GU. 4) The GST rate cut will impact annual incentive run-rate by Rs130-150/t; Star expects to accrue Rs1.5-1.8bn worth of annual incentives over FY26-28. 5) Cement price in the Northeast is flat as of Q3FY26TD vs end-Q2FY26; Star expects a similar pricing buoyancy, as entry of a new player in the Northeast in the next ~4Y is unlikely. 6) The Northeast remains one of the fastest cement consuming regions, with ~10% medium-term CAGR backed by infrastructure spends of Central/State governments.

We like Star’s regional dominance and endeavor toward stretching its leadership over peers in the northeastern market. Further, entry into Rajasthan will help it shed the tag of a regional player and establish its brand in North India too, coupled with >2x its existing capacity base. At CMP, Star trades at ~10x FY27E EV/EBITDA, viz close to the 5Y mean. We maintain BUY on the stock as well as our earnings estimates; we retain TP of Rs280.

With home turf guarded well, Star likely to look to diversifying in North India Star already commands ~27% volume market share in the Northeast which will be boosted by commissioning of the Silchar GU in H2FY26E. After commissioning of the Silchar GU, Star will look to execute the 2mtpa Bihar GU, followed by the greenfield integrated unit at Nimbol, Rajasthan. Star plans setting up a 2.8-3.3mtpa clinker line at Nimbol, along with a 2-2.5mtpa GU. Further, a 2-2.5mtpa satellite grinding unit at Barwala, Haryana is planned, for catering to the fast-growing markets of NCR, Punjab, and Haryana. Post Nimbol, Star has already secured 271mnt of limestone reserves along with plant land at Jaisalmer, Rajasthan, for its phase-II expansion in North India.

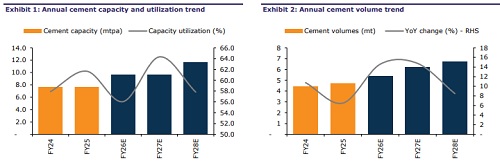

Enough dry powder to support capacity expansion to ~18mtpa in 4-5 years Star, with current capacity base of 7.7mtpa, will commission its 2mtpa GU at Silchar, Assam in Q4FY26. Following this, it will look to commission another 2mtpa in Begusarai, Bihar at a capex of ~Rs5bn. Subsequently, Star is likely to pick up a project in Rajasthan (4/5mtpa IU expansion at ~Rs25bn capex), followed by a greenfield IU project in Umrangso, Assam. We estimate Star’s cumulative operating cash flows at ~Rs25bn over FY26E-28E, along with likely fund-raise of ~Rs15bn providing enough liquidity to support >2x capacity expansion in the next 4-5 years.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354