2025-04-10 12:23:40 pm | Source: Motilal Oswal Financial Services Ltd

Buy Shriram Finance Ltd For Target Rs. 775 by Motilal Oswal Financial Services Ltd

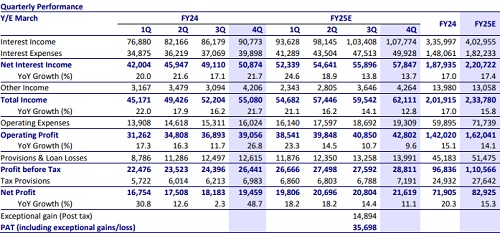

* Estimate disbursements of ~INR453b, leading to AUM of ~INR2.65t (up 18% YoY/ ~4% QoQ).

* Credit cost is likely to remain stable QoQ at 2.2%.

* Margin is expected to contract ~10bp QoQ to 8.9%.

* Commentaries on loan growth in CV and on asset quality in 2W and PL segments are the key monitorables.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Disclaimer:

The content of this article is for informational purposes only and should not be considered financial or

investment advice. Investments in financial markets are subject to market risks, and past performance is

not indicative of future results. Readers are strongly advised to consult a licensed financial expert or

advisor for tailored advice before making any investment decisions. The data and information presented

in this article may not be accurate, comprehensive, or up-to-date. Readers should not rely solely on the

content of this article for any current or future financial references.

To Read Complete Disclaimer Click Here

Latest News

National e-Governance conference: PM Narendra Modi's...

Evening Roundup : Daily Evening Report on Bullion, B...

NHAI one step closer towards barrier-free commuting ...

Monthly Choice :- Buy DELHIVERY in Cash @ 500.4 SL 4...

Market Commentary (closing) for 01st July 2026 by Ba...

Quote on Technical Market Commentary for July 1st , ...

Sell Gold Below 140500 SL ABOVE 141500 TGT 139000/13...

Quote on Daily Market Commentary for July 1st , 2026...

The index opened on a positive note and initially ex...

Edelweiss AMC Crosses Rs 1 Lakh Crore Equity AUM Mil...