2025-10-15 04:35:04 pm | Source: Motilal Oswal Financial Services Ltd

Buy Maruti Suzuki Ltd for the Target Rs. 18,501 by Motilal Oswal Financial Services Ltd

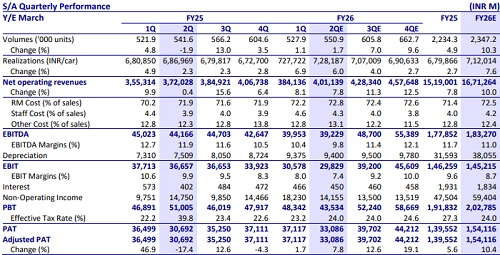

* MSIL reported just 2% YoY growth in volumes due to challenging demand in domestic market for bulk of 2Q. Exports mix improved 200bp QoQ to 20%.

* EBITDA margin to be under pressure at 9.8% (-210bp YoY) as benefits from operating leverage are likely to be more than offset by higher discounts and new launch expenses QoQ.

* We expect MSIL to post 8% YoY growth in PAT in 2Q.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Disclaimer:

The content of this article is for informational purposes only and should not be considered financial or

investment advice. Investments in financial markets are subject to market risks, and past performance is

not indicative of future results. Readers are strongly advised to consult a licensed financial expert or

advisor for tailored advice before making any investment decisions. The data and information presented

in this article may not be accurate, comprehensive, or up-to-date. Readers should not rely solely on the

content of this article for any current or future financial references.

To Read Complete Disclaimer Click Here

Latest News

Mergers and acquisitions? deal value in India jumps ...

Nifty, Sensex post strong weekly gains over sustaine...

LokOS digital platform boosts 'Lakhpati Didi' initia...

Kakao Ventures eyes massive returns amid renewed glo...

India, France to boost cooperation in critical miner...

India's AI-ready workforce, industry-led skilling ma...

In a first, 40 tonnes of Varanasi biscuits exported ...

Commentary on Weekly FII and DII 04th July 2026 by P...

India's maritime sector entering a defining decade o...

'Sanand has earned global recognition': PM Narendra ...