Buy Samhi Hotels Ltd for Target Rs.200 by Choice Institutional Equities

Strategic Asset Revamp driving SAMHI’s Upper-upscale Expansion

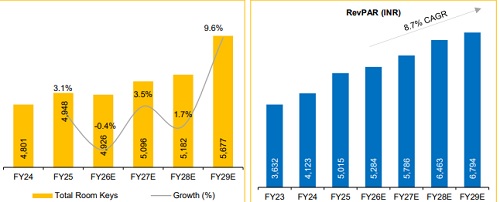

SAMHI, by FY29E, is expected to operate 5,677 keys across its key micromarkets, strategically located around corporate corridors and major air-traffic hubs. Its acquisition-and-rebranding strategy, accounting for nearly 87% of its portfolio, has been the centre of this growth engine, enabling the turnaround of underperforming assets under global brands, while the remaining 13% adds steady performance support. With planned expansions, rebranding, and conversions to upper-upscale inventories, we expect ARR growth CAGR of 7.7% and a revenue CAGR of 14.3% over FY26E–29E, reaffirming SAMHI’s position as a high-efficiency consolidator in India’s premium hospitality market.

Efficiency, F&B Ramp Up and Upgrades to Boost Margin

SAMHI’s profitability is poised to strengthen further, supported by disciplined cost structure, improving revenue mix, and operational upgrades. The company operates with lean employee costs (~17% of revenue) and controlled OTA bookings exposure (16%), keeping commissions low at ~4.2% of sales. This cost discipline, coupled with a rising share of highmargin room revenue (~60%) and improving F&B performance, continues to enhance operating leverage. Additionally, the transition of ACIC portfolio assets to managed operations and the ongoing upgrade of select ‘Four Points’ hotels to the Upscale category are expected to boost margin by 388 bps by FY29E

Unlocking Value: Leveraging Capital and Assets Sale for Expansion

SAMHI’s strategic capital approach, anchored on the GIC infusion of INR 7.5 Bn and asset monetisation of INR 2.1 Bn, has significantly deleveraged the company. This has lowered net debt-to-EBITDA to 2.9x, reduced the effective interest rate to ~8.3%, and materially boosted free cash flow from INR 577 Mn in FY25 to INR 2.4 Bn in FY29E for reinvestment and growth. This strategy, through targeted asset rebranding, has led to a 33% lower capex per key, creating a self-funding growth engine, allowing SAMHI to fund expansion primarily through internal accruals. We believe this approach is expected to reduce finance cost by a CAGR of 19.8% over FY26E–FY29E, leading to a PAT CAGR of 22.1% over FY26E–FY29E.

View and Valuation: We initiate coverage on SAMHI with a BUY rating and an FY28E EV/Adj. EBITDA of 9x to arrive at a TP of INR 200, implying an upside potential 49.1%. We expect SAMHI to deliver Revenue / EBITDA / PAT CAGR of 14.3% / 18.2% / 22.1% over FY26E–29E, driven by the acquisitionand-rebranding model, ongoing premiumisation and a self-funding growth platform.

Optionality: SAMHI’s stake in RARE India positions it to build a scalable asset-light experiential platform with ~INR 900–1,000 Mn revenue potential

Key Risks: Extended Geopolitical Conflict, Exposure to leverage, interest rate volatility, execution risk in asset turnarounds, operator dependence, and land title uncertainties.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

.jpg)