Buy Rubicon Research Ltd For Target Rs.1,160 by Motilal Oswal Financial Services Ltd

Another quarter, another beat: The compounder delivers R&D productivity, Arinna, and the US brand fuel the next leg of growth

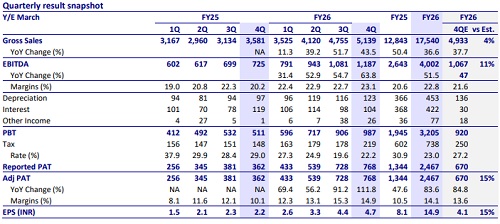

* Rubicon Research (Rubicon) delivered another outstanding quarter, beating revenue, EBITDA, and PAT estimates by 4%, 11%, and 15%, respectively. Growth was well-diversified, driven by healthy momentum from recent launches alongside sustained traction in the existing portfolio.

* Commercialization quality was strong, with 92% of approved products generating revenue, while pricing stability was aided by Rubicon's differentiated product focus. Specialty products maintained a steady contribution of 32.8% to gross profit, reaffirming the structural shift in portfolio mix.

* On R&D productivity, Rubicon exited FY26 at 5.9x, which was measured as incremental revenue in FY26 over R&D spending across FY22, FY23, and 1QFY24. Management remains confident of sustaining 5x+ productivity going forward, reflecting the compounding returns from its innovation pipeline.

* Working capital efficiency improved meaningfully, with net working capital days declining from 137 in FY25 to 126 in FY26 — a noteworthy achievement considering the deliberately elevated inventory levels maintained to capture near-term demand opportunities.

* For Arinna Lifesciences integration, management has outlined a phased approach. Phase 1 and 2 will prioritize revenue scale-up with a target of outperforming IPM growth by FY28, while Phase 3 will shift focus towards profitability improvement.

* We marginally raise our earnings for FY27/FY28. Rubicon has delivered an exceptional 54% revenue CAGR over FY22–26, with gross profit compounding at 50% over the same period. The company has transformed from an EBITDA loss of INR392m in FY22 to INR4b in FY26 — a testament to the consistent and disciplined R&D investment cycle. The outlook remains equally compelling, with multiple growth levers in place: differentiated products within the US generics space, prescription-led brand building in the US market, and domestic formulation scale-up through Arinna. We expect earnings to compound at 30% over FY26–28.

* Given the strong track record, robust earnings compounding outlook, and superior return ratios, we expand our P/E multiple to 45x (from 37x previously), arriving at our revised TP of INR1,160. Reiterate BUY

Highlights from the management commentary

* Rubicon is witnessing broad-based demand across the portfolio for products that have been in the market for a few years now, as well as the recently launched products.

* Management guided a 22-23% EBITDA margin for FY27, factoring in the Pithampur-related opex, ESOP expenses, and Arinna-related expenses, as well as any RM cost/logistics cost escalation.

* While net working capital (NWC) days have reduced from 137 to 126, management indicated NWC days to be in this range (~126) to ensure adequate inventory levels for existing products and upcoming launches.

* Products are filed from the site acquired from Alkem, and Rubicon awaits USFDA inspection. Ramp-up of production from 1QCY27 is on track as guided earlier.

* Strategically, the acquisition of Arinna Life is the extension of go-to-market and not the shift of focus to an alternate geography.

* Rubicon is targeting outperforming IPM growth for the Arinna business by FY28.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412