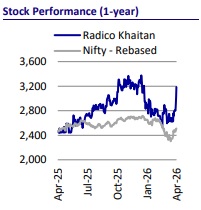

Buy Radico Khaitan for the Target Rs.3,850 by Motilal Oswal Financial Services Ltd

Radico Khaitan (RDCK) has scaled at a pace far superior to the industry over the years, resulting in market share gains (31m cases vs ~400m industry size in FY25; ~8% share). A sharper shift is witnessed in P&A volumes, which have expanded from ~4m cases in FY15 to ~17m cases in FY26E, materially boosting RDCK’s earnings profile. P&A contributes ~70% of IMFL revenues (vs ~48% in FY19), which is expected to increase further, backed by premiumization and operational efficiencies.

The Indian liquor industry continues to witness steady demand growth, supported by favorable demographics, increasing income, and social acceptance. This tailwind is also visible in operating performance, with IMFL and P&A volumes each growing ~30% in 9MFY26, significantly ahead of historical industry growth. Further, the recent liquor policy in most markets was positive for the alcobev industry.

RDCK has been a key beneficiary of this shift. Its P&A portfolio delivered 13% volume CAGR over FY19-25 (20% revenue CAGR), with a steady improvement in the category mix. The company’s super-premium and Scotch segments are witnessing strong traction, driving higher realizations per case through a rising share of premium brands. RDCK’s premium portfolio, led by Rampur, Jaisalmer, and Royal Ranthambore, contributes ~10% of IMFL sales (INR3.4b in FY25) and is expected to scale to INR5b in FY26, supporting the company’s premiumization-led growth strategy.

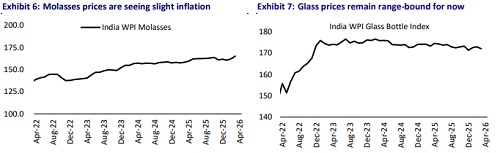

The liquor industry cost structure is relatively insulated from crude volatility, with ENA (30-35% of RM cost) majorly being domestically procured. Glass, another key input (~25% of RM cost), has only an indirect energy linkage, limiting direct impact from crude/LPG inflation. RDCK’s backward integration (Sitapur distillery) ensures a healthy ENA supply and increased use of recycled glass (4.5% in FY19 to 19.8% in FY25), help it effectively control costs. This makes RDCK’s earnings relatively resilient compared to other consumption categories that are sensitive to crude derivatives.

Over FY22-24, RDCK’s margins were under pressure due to sharp inflation in key inputs such as ENA and glass (EBITDA margin contracted from 17% to 12%). Going forward, RDCK’s margins are expected to expand gradually, supported by premiumization-led mix improvement, stable raw material pressures, and operating leverage from scale benefits. Further, structural cost benefits from initiatives such as packaging optimization and potential savings from the India-UK FTA are likely to support margins. The company expects a 125-150bp margin expansion each year for the next three years, and we model a 75bp yearly expansion.

RDCK has been outperforming UNSP, driven by higher growth in its P&A portfolio. The company’s P&A volumes rose ~2.7x vs ~1.3x of UNSP over FY19-26E, while P&A revenue rose 3.8x vs. 1.9x. This superior growth trajectory has translated into a meaningful valuation re-rating, positioning RDCK as a fast-compounding challenger.

RDCK’s debt is declining steadily, supported by a healthy free cash flow generation. The company has reduced net debt by INR2.1b since Mar’25 and is on track to be debt-free by FY27-end. It continues to deliver strong growth in its P&A segment, with premiumization remaining a key structural driver. The luxury and semi-luxury portfolio continues to grow at a healthy pace, supported by new launches and rising consumer demand. RDCK is currently trading at 56x/46x FY27E/FY28E P/E, with RoE/RoIC of 18%-20%. We believe that ~25% EPS CAGR over FY26-28E provides adequate support for sustaining rich valuations. We value the company at 55x FY28E EPS to derive a TP of INR3,850 and reiterate a BUY rating on the stock.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

600-400.jpg)