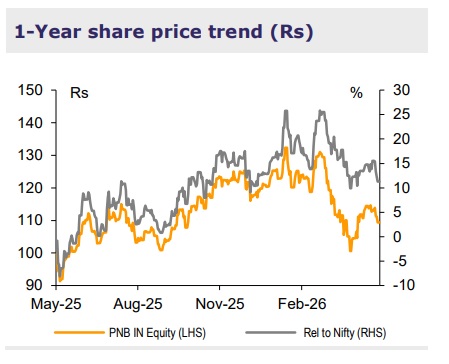

Buy Punjab National Bank For Target Rs.135 By Emkay Global Financial Services Ltd

PNB logged an earnings miss, with PAT at Rs52bn mainly due to continued contraction in margins and lower treasury gains, albeit partly offset by lower staff costs benefiting from yield movement on retirement liability. Credit growth remains moderate at 13.7% YoY/2.4% QoQ. PNB has made Rs2.7bn of floating provisions to absorb the ECL impact from 1-Apr-27, with cumulative buffer now at Rs20.5bn/0.2% of loans. For FY27, the management expects credit growth to be rangebound, while indicating there is no visible stress in the book on account of the West-Asia conflict; it expects announcement of government support soon, though. PNB aims to rebalance its loan mix by reducing corporate share, from ~46–47% to ~42% in the near term (LT: 40%) while increasing RAM (Retail, Agri, MSME) to ~58% in FY27 and to ~60% in the LT; this is likely to support NIM, which is otherwise an irritant. Factoring in moderate growth, margins and pressure on treasury, we trim our earnings estimate by 5-7% and lower our TP by 10% to Rs135 from Rs150 (based on 0.9x FY28E ABV and subsidiary/investment value at Rs10/sh. However, given cheap valuations, we retain BUY.

Margins continue to slip

PNB reported healthy credit growth of 13.7% YoY/2.4% QoQ, driven by the low-yielding overseas corporate book and MSME segments, while retail growth remained moderate at 9% YoY. Deposit growth stood at ~9.0%, with CASA stable at 35.6%. Moderating retail growth, along with the full-quarter impact of the December rate cut and sticky deposit pricing, led to a 5bps decline in NIM to 2.47%. The bank expects NIM to improve toward 2.6–2.7%, supported by easing incremental deposit costs (down by ~2–3bps monthly and ~5bps over Q1–Q2) and a favorable mix shift toward higher-yielding RAM assets. It also aims to rebalance its portfolio by reducing corporate exposure, from ~46–47% to ~42% in the near term (long term: 40%) while increasing RAM share to ~58% this year and to ~60% over the long term.

Seasonally higher agri slippages; bank further builds in ECL buffer

Gross slippages rose to Rs27.6bn (1.0% of loans) mainly due to seasonally high agri slippages; however, higher write-offs along with steady recoveries and upgrades led to a 24bps improvement in GNPA to 2.95%. Specific PCR remained strong and stable at 90%, resulting in a lower NNPA of ~0.3%. The management sees no visible stress in the book and is proactively engaging exporters and importers to address any emerging risks from the West-Asia conflict. PNB now carries a healthy floating provision buffer, to the tune of Rs20.5bn/0.2% of loans, to limit the impact of ECL, once implemented by 1-Apr-27.

We retain BUY while revising down our TP to Rs135

Considering moderate growth, margins, and pressure on treasury, we trim our earnings estimate by 5-7% and cut our TP to Rs135 (based on 0.9x FY28E ABV + subs/investment value at Rs10/sh). However, given cheap valuation, we retain BUY. Key risks: Macro deterioration derailing growth, asset-quality normalization, ECL implementation.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354