Buy Lodha Developers Ltd for the Target Rs. 1,150 by Motilal Oswal Financial Services Ltd

Well-placed for a diversified scale up

Pre-sales momentum expected to remain healthy

In 4QFY26, Lodha Developers’ (LODHA) pre-sales grew by 23% YoY to INR58.9b (in line), supported by sustenance inventory as well as new launches of ~6.7msf (GDV ~INR140b). This was driven by a robust 58% YoY pre-sales growth in the South & Central micro-market (39% contribution). Overall, FY26 pre-sales grew 16% YoY to INR205b, which was a marginal 2% miss on the initial guidance due to slower NRI sales in the luxury segment. For FY27, a launch pipeline of ~15msf (GDV ~INR218b), INR514b unsold inventory (~30months; healthy), and future pipeline of 72msf beyond FY27 can keep the growth engine running for the medium term, even if business development remains muted in the next 2Y. Based on the assumption of the Middle East situation normalizing by 1QFY27-end, the company has guided for 17% YoY pre-sales growth in FY27. We expect a 16% CAGR in pre-sales to INR275b during FY26-28E, with an improving regional diversification, as the NCR project is also expected to be launched in 4QFY27/1QFY28.

Business development acceleration improves growth visibility

The company sharply accelerated its business development with the addition of INR601b GDV in FY26, which is equivalent to 75% of the total BD done during FY22-25. However, this has come along with regional diversification, as ~27% of the BD in FY26 came from outside MMR: NCR (INR33b; 2 projects), Bengaluru (INR106b; 2 projects), and Pune (INR25b; 1 project). Given the aggressive BD in FY26, new additions are expected to be more selective and slower over the next 2Y. However, the company currently has ~INR2t GDV available for sale (excluding long-term township land), which lends comfort on growth visibility over the medium term.

Strong collections growth; leverage well under control

In 4QFY26, collections grew by 18% YoY to INR52b, supporting healthy OCF of ~INR30b. Net debt reduced by INR8b QoQ to INR54b (net D/E @0.23x). In FY26, despite INR68b deployment toward growth in DevCo and INR6.8b in RentCo, net debt increased by ~INR14b, given the strong ~INR71b OCF generation. With moderating BD in the next 2Y, LODHA expects strong FCF generation. DevCo is also expected to deleverage toward a net debt-zero position over the medium term, while internal accruals and proceeds from land sale would be deployed toward the scale-up of the data center business.

Financial performance

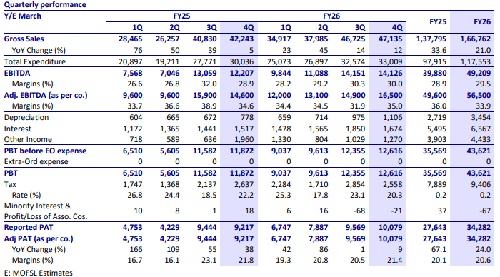

In 4QFY26, LODHA’s revenue grew 12% YoY to INR47b. EBITDA grew by 16% YoY to INR14b, while EBITDA margin was at 30%. Adjusted EBITDA grew 13% YoY to INR16.5b, whereas margin was at 34%. Adjusted PAT was broadly flattish YoY at INR10.1b (20% margin). In FY26, revenue grew by 21% YoY to INR166.8b. EBITDA grew by 23% YoY to INR49.2b, with EBITDA margin at 30%. Adjusted PAT grew by 24% YoY to INR34b, with a 21% margin. The company expects a 20% CAGR in PAT to INR85b+ during FY26- 31.

Valuation and view

* Along with an increasing scale, LODHA has showcased its ability to diversify well regionally outside the MMR, which is expected to increase the opportunity size, derisk the operational performance, and improve growth visibility over the medium term. Further, the disciplined cash flow generation has ensured the continued addition of new projects to the portfolio vis-à-vis keeping leverage well under control and balance sheet strength under check. On the back of presales performance as well as project execution, we expect collections growth and OCF generation to remain strong over the next 2-3Y. Scale up in the commercial segment and data center businesses would offer additional avenues for growth over the medium term.

* The company is trading at a 29% discount to its residential segment NAV. We have valued the Devco at its NAV, whereas the annuity business is on 7.5% cap rate.

* We have a BUY recommendation with a TP of INR1,150.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412