Buy Persistent Systems For Target Rs.4280 by Elara Capital

Higher costs drag margins

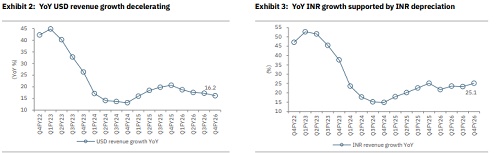

Persistent Systems’ (PSYS IN) Q4 revenue was largely in line but EBIT margins were below our estimates due to higher-than-expected costs. The company ended FY26 at 17.4% USD revenue growth. It continues to maintain its guidance of USD 2bn annualized revenue by Q4FY27 and USD 5bn by FY31. Though PSYS has minimal exposure to the Middle East, the management sounded cautious regarding the growth of its US market (>80%+ mix) in the medium term, given the war may continue for the long term thus pushing inflation higher in that market. As per our calculation, the ask rate to reach FY31 target is 3.5% CQGR (organic). The company ended FY26 at 15.6% EBIT margin. Management had earlier guided for healthy medium-term margin expansion of 150-200bps, but it now appears to be prioritizing growth over margin expansion. We maintain SELL with a lower TP of INR 4,280 (unchanged multiple of 26x).

Broad-based growth across verticals: PSYS reported a growth of 3.4% QoQ in CC terms and 3.2% in USD terms in Q4. In INR terms, growth was 7.4% QoQ and 25.1% YoY. In Q4, growth was led by North America and India, as revenue from these markets rose 3.1% QoQ and 9.8% QoQ, respectively, followed by RoW at +3.2% QoQ. Europe market continues to be a drag on growth, declining 1.7% QoQ. Vertical-wise, growth was led by Healthcare, up 6.9% QoQ, followed by Hi-Tech, up 2.2% QoQ. BFSI grew 1.7% QoQ in USD terms in Q4FY26. TCV came in at USD 600.8mn, -10.9% QoQ/+16.1% YoY, while annual contract value (ACV) came in at USD 445.1mn, -11.3% QoQ/+27.1% YoY. LTM attrition was down 50bps QoQ to 13.0%, while PSYS reported a net addition of 791 employees in Q4. Utilization was down 40bps QoQ to 88% in Q4 The Board declared an interim dividend of INR 18 per share, with total dividend for FY26 at INR 40 per share and a payout ratio of 33.6%.

Margin contraction led by increase in sub con costs: Q4 EBIT margin was down 40bps to 16.3%, impacted by higher consulting and advisory costs linked to corporate development initiatives (-60bps) and increased subcontracting, software license purchases, and travel related to the annual planning cycle (-70bps). These were partially offset by tailwinds, including favorable currency movement (+60bps) and operational efficiencies. PSYS is targeting an aspirational range of 16–17% EBIT margins in the medium term, while prioritizing growth and continued investment in AI platforms, talent, and partnerships.

Maintain SELL with a lower TP of INR 4,280: PSYS continues to report a broad-based growth across all customer segments. BFSI reported strong growth in FY26 due to expanding relationship with existing clients as well as the addition of new clients. Healthcare reported relatively weak growth due to funding constraints for clients in the US. We are building in 14.1%/15.3% USD /INR revenue growth CAGR in FY26E-28E, largely in line with the long-term guidance. We expect some pressure on profitability due to elevated costs and hence, cut our earnings estimates by 4-5% for FY27E/28E. Accordingly, we cut our TP to INR 4,280 (from INR4,430). We maintain SELL on PSYS at an expensive valuation (the stock is trading at 37x and 32x on FY27E/FY28E).

Please refer disclaimer at Report

SEBI Registration number is INH000000933