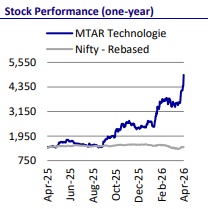

Buy MTAR Technologies Ltd for the Target Rs.6,000 by Motilal Oswal Financial Services Ltd

The expanded strategic partnership between Oracle and Bloom Energy (Bloom) to 2.8GW (from 1.2GW) underscores Bloom’s capability to provide fast and reliable power suited for AI workloads, which require rapid, load?following support that traditional grids were not designed to deliver. This additional order can translate into ~INR14-17b incremental orders for MTAR Technologies (MTARTECH)—i.e., 1.6-1.8x of its FY26E revenue.

* Building on the theory of fuel cell growth and aligning with global data center expansion as per our last report, we are factoring in strong order visibility for MTARTECH’s fuel cell business. We, thus, raise our revenue growth estimates for this business by 16%/33% for FY27/FY28. This translates into a 14%/25% upward earnings revisions for FY27E/FY28E.

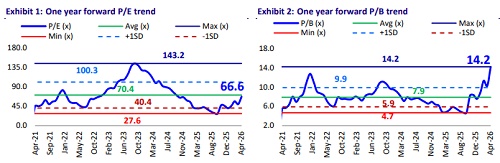

* We now forecast a revenue/EBITDA/PAT CAGR of 49%/65%/90% over FY25-FY28. We reiterate our BUY rating on MTARTECH and raise our TP to INR6,000, valuing the stock at 50x FY28 EPS (i.e., ~0.65x PEG on FY25-28E EPS CAGR).

Bloom and Oracle firm up their partnership

* Bloom has expanded its partnership with Oracle to support the rapid buildout of AI and cloud infrastructure in the US.

* Under a master agreement (explained below), Oracle plans to procure up to 2.8 GW of Bloom’s fuel cell systems, with an initial 1.2 GW already contracted and currently being deployed (by 2027).

* Bloom’s fast-to-install modular systems provide reliable onsite power for energy-intensive AI data centers, helping Oracle meet rising demand while reducing deployment time and project risk.

* The deal follows a successful earlier installation completed in just 55 days and strengthens both companies’ shared vision for future energy and AI infrastructure.

* They have structured their relationship as both a commercial supply agreement and a strategic equity-linked partnership, designed to accelerate Oracle’s AI/data-center expansion while giving Blooms long-term revenue visibility.

* Commercial Contract: Alongside the supply agreement, Bloom issued stock warrants to Oracle (announced on 30th Oct’25). A warrant provides Oracle with the right to buy Bloom’s shares at a fixed price in the future, usually tied to commercial milestones. Reported terms indicate Oracle received warrants for roughly 3.5m Bloom shares at an exercise price near USD113.28 (subject to exact legal terms and vesting conditions).

* Why use a warrant structure? For Oracle, it provides upside potential if Bloom’s stock rises significantly, aligning Oracle’s interests with Bloom’s success. It also reduces the effective cost of large procurements over time. For Bloom, it secures a marquee hyperscaler customer, guarantees substantial future orders, avoids immediate cash discounts, and generates a strong signaling effect for other hyperscalers.

* This 2.8GW contract can translate into multi-billion-dollar revenue potential for Bloom over several years, depending on pricing, service revenue, installation timing, and mix.

An order win for Bloom, incremental revenue for MTARTECH

* As discussed earlier, the correlation of Bloom’s order wins and MTARTECH’s incremental flows (i.e., 1GW of orders for Bloom translates into INR9-11b of revenue for MTARTECH). This order win translates to INR14-17b incremental revenue potential (1.6-1.8x of FY26E revenue) for MTARTECH over the next few years.

* Factoring this in, we raise our revenue projections for FY27/FY28 by 16%/33% for the clean energy fuel cells business.

* This rise in revenue is in line with the capacity expansion undertaken by the company. We expect MTARTECH to deliver ~9,700/14,000 hot boxes in FY27/FY28 (i.e., ~0.63/0.91GW), which is ~61%/56% of its utilization levels (refer to Exhibit 5).

* The increased revenue from clean energy is expected to increase its contribution to the overall business to 71% by FY28 vs. 62% in FY25 (indicating higher client concentration risk). However, in the current scenario of macro tailwinds, this is acting as a growth catalyst for the company.

* The key risk to the growing fuel cell business is the higher working capital requirement. MTARTECH may need additional short-term funding through internal cash flows, supplier credit, or bank working-capital lines to finance inventory and receivables growth.

* If the orders suddenly ramp up in the current scenario, the working capital needs can rise materially before profits are realized. However, if MTARTECH negotiates milestone advances, faster payment cycles, or vendor credit from suppliers, the pressure can be reduced significantly.

Valuation and view

* The global AI infrastructure buildout has created a singular and structural demand shock — one where power availability, not capital, has become the defining constraint for data center expansion. Bloom has uniquely positioned itself as the fastest and most reliable solution to this bottleneck.

* MTARTECH, as Bloom's key supplier of critical hot box assemblies (commanding 60-70% wallet share), is not merely a beneficiary of this theme but an irreplaceable enabler of it.

* We remain bullish on this long-term growth trajectory for MTARTECH, which presents a rare combination of structural positioning, earnings visibility, and exponential order growth, all anchored by a decade-long, deeply entrenched customer relationship that is difficult to replicate.

* We are factoring in strong ordering visibility for the fuel cell business of MTARTECH and raising our revenue growth estimates for this business by 16%/33% for FY27E/FY28E. This translates into an upward earnings revision for FY27E/FY28E by 14%/25%.

* We now forecast a revenue/EBITDA/PAT CAGR of 49%/65%/90%. We reiterate our BUY rating on MTARTECH and raise our TP to INR6,000, valuing the stock at 50x FY28 EPS (i.e., ~0.65x PEG on FY25-28E EPS CAGR).

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041