Buy Engineers India Ltd For Target Rs.255 by Prabhudas Liladhar Capital Ltd

Infra & overseas pulse strengthens EIL’s rhythm

Quick Pointers:

* The management has guided revenue growth of 20%+ for FY26 with Consultancy/LSTK margins of ~25%/5-7%.

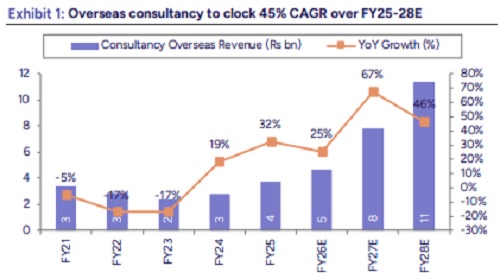

* Strong traction seen in overseas hydrocarbon consultancy as EIL expands into new geographies like Mozambique, Tanzania and Egypt.

We interacted with the management of Engineers India (EIL) to discuss the company’s financial and operational performance, expansion into new geographies, and growth outlook. EIL continues to strengthen its margin profile by strategically lifting the share of high-value consultancy (targeting 50-55% of order intake) while being selective in executing lower margin LSTK projects. Diversification into non-O&G continues to scale with clear focus on niche and engineering-intensive infra projects such as airports, data center and institutional infra. Overseas momentum remains strong with good traction for hydrocarbon consultancy projects across the Middle East and Africa. Stabilization of RFP and NRL assets is expected to generate strong cash flow by FY27, supporting the mandated 30% dividend payout. With a healthy domestic hydrocarbon capex cycle, expanding consultancy intensity, and strengthening overseas footprint, EIL remains well positioned for sustained, multi-year growth. The stock is currently trading at PE of 15.1x/12.7x on FY27/28E. We reiterate our ‘BUY’ rating valuing the Consultancy/Turnkey segment at PE of 22x/10x Sep’27E (same as earlier) arriving at SoTP-derived TP of Rs255 (same as earlier).

Long-term view: We believe EIL’s long-term growth prospects remain intact given the

1) strong order book prospects in non-O&G and O&G projects;

2) strong traction in overseas consultancy business from the Middle East and Africa region;

3) opportunities in energy transition & infrastructure; and 4) lean balance sheet.

Key takeaways from management interaction

Overseas business scaling up with margin focus

* Overseas business remains entirely consultancy-led, focused on high-margin hydrocarbon assignments.

* The management highlighted that the Abu Dhabi continues to perform well, supported by a strong pipeline, while Saudi Arabia is scheduled to open this year, with meaningful business ramp-up expected from FY27.

* The UAE remains its largest international market with ~Rs10bn of orders, reinforcing EIL’s positioning in the region.

* In Africa, Nigeria remains an active geography, with follow-on consultancy opportunities emerging.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271