Buy Marksans Pharma Ltd For the Target Rs. 310 by Choice Broking Ltd

All-time high and in-line quarterly Revenue, EBITDA, and PAT; EBITDA margin impacted due to investment in the TEVA facility

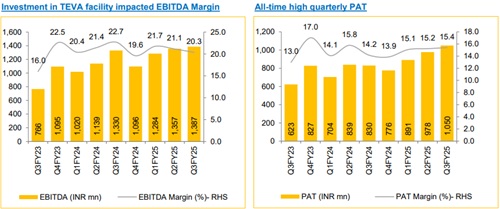

* Revenue came at INR 6.8 Bn (vs. CEBPL est. of INR 7.1 Bn), up 16.3% YoY and up 6.2% QoQ.

* EBITDA came at INR 1.4 Bn ( vs. CEBPL est. of INR 1.6 Bn), up 4.3% YoY and up 2.2% QoQ. EBITDA margin came at 20.3% (vs. CEBPL est. of 22.5%), contracted by 235bps YoY and 79bps QoQ.

* PAT came at INR 1.1 Bn (vs. CEBPL est. of INR 1.1 Bn), up 26.6% YoY and up 7.4% QoQ, with a PAT margin of 15.4% (vs 14.2% in Q3FY24).

Growth supported via acquisition and ramping-up of TEVA facility

MRKS aims to drive growth through strategic acquisitions, particularly in the European market(38% of revenue), as well as other growth markets. The company plans to expand its market presence by acquiring front-end marketing and distribution companies. We expect the growth to be achievable due to a strong balance sheet of around INR 6,500 Mn. of cash. Continuous focus on R&D and capacity expansion by acquiring TEVA facility will support the launch of new products in the pipeline. The facility is currently generating INR 4,500 Mn. of revenue which is expected to achieve INR 6,000 Mn. by FY26. We expect that the TEVA facility will help supplement the growth, by new product launches and enhancing supply management.

Doubling revenue in the US and North America market; from 9 Bn. to 18 Bn. by FY27

During the quarter, US outpaced the company's overall growth, more than doubling the company's revenue growth, supported by introduction of new products and increased market share. We expect that the doubling of US revenue will be supported by leveraging product launches, supply chain efficiency, and leveraging its low-cost manufacturing base in India to supply the US market. In FY24, US contributed 42% of the total revenue which is expected to be around 50% by FY27. The company target of achieving revenue of INR 30,000mn by FY26, with major growth coming from US market

View and Valuation:

We anticipate the company’s growth will be driven by expanding the OTC business (high-margin compared to prescription), aiming to double revenue in the US market, healthy product pipeline (76 products), backward integration to improve margins, growth via acquisitions, and expansion of TEVA facility. We maintain our BUY rating with a revised target price of INR 310 valuing on 23x of FY27E EPS (earlier 30x, revised due to US uncertainties), reflecting a CAGR of 18.2%/21%/24.7% for revenue/EBITDA/PAT over FY24-27

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131