Buy Marico Ltd for the Target Rs. 875 by Motilal Oswal Financial Services Ltd

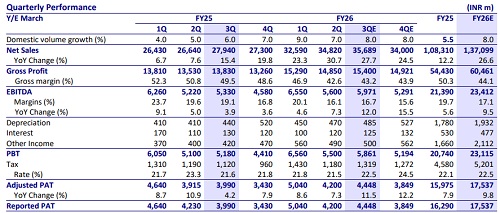

* In the pre-quarter update, MRCO estimated high-single digit volume growth (est. +8%) in the India business. Consolidated revenue grew in the high 20s (est +28%).

* GM is expected to improve sequentially (est. 43.2% in 3Q, up 60bp QoQ) and EBITDA will grow in double digits (est. +12% YoY).

* Parachute volume declined marginally. Saffola Oils has muted quarter. VAHO grew in the 20s. Foods had a benign quarter, while premium personal care showed resilient growth.

* The International business is expected to deliver revenue growth (CC terms) in the early 20s.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Retail Sector Update : QSR - QSR at an inflection point; risk-reward favorable By Motilal O...