Buy Marico Ltd For Target Rs. 825 by Motilal Oswal Financial Services Ltd

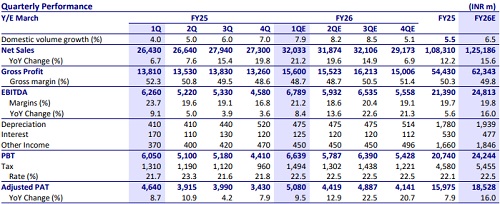

* The domestic business is experiencing steady improvement. We expect 21% consol. revenue growth and ~8% domestic volume growth. The high pricing contribution is driven largely by price hikes in Parachute.

* Gross margins expected to contract 355bp YoY to 48.7%, given the high base and rise in RM prices. Operating margins are expected to contract 250bp YoY to 21.2%.

* Parachute oil is expected to deliver >20% revenue growth, aided by pricing interventions as the company incorporated another round of price hike in Jun’25. Saffola oil is expected to deliver revenue growth in the high twenties, backed by mid-single digit volume growth. Moreover, VAHO revenue grew in low double digits.

* The International business is expected to deliver revenue CC growth in high teens, with positive contributions from all markets.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Retail Sector Update : QSR - QSR at an inflection point; risk-reward favorable By Motilal O...