Buy Leela Palaces Hotels and Resorts Ltd for Target Rs. 510 by Choice Institutional Equities

Pure-play Luxury Platform, Backed by Brookfield

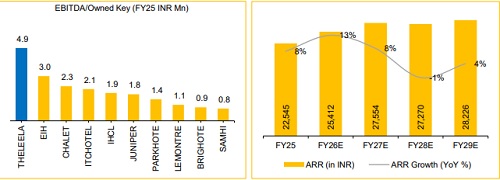

THE LEELA, backed and majority-owned by Brookfield (~USD 1 Tn AUM), operates as India’s only institutionally owned pure-play luxury hospitality platform. Brookfield’s long-term capital and governance discipline has enabled THE LEELA to scale a portfolio of five owned palace hotels across Udaipur, Jaipur, Chennai, Bengaluru and Delhi, along with eight managed luxury properties across key urban and leisure markets. The owned portfolio comprises some of India’s most iconic luxury assets, supporting one of the highest ARRs in the country. ARR stood at ~INR 22,500 in FY25 (~2.7x the Indian industry average) and is expected to scale to ~INR 27,500 by FY29E. Premium positioning translates into stable occupancy (68 - 72%) and industryleading EBITDA per owned key of ~INR 4.9 Mn in FY25.

Robust Pipeline of Marquee Luxury Assets in Iconic Markets

As of end-H1FY26, THELEELA operated a portfolio of 3,544 luxury keys. The company has commenced its first international expansion through a strategic investment in a Dubai luxury hotel adding ~546 keys (including 182 residence keys) and an acquisition of resort in Coorg adding 71 keys, taking its total current inventory to ~4,161 keys. Concurrently, THELEELA is entering one of India’s most underserved hospitality corridors at Bandra - Kurla Complex (BKC), Mumbai, with a planned 250-key owned ultra-luxury hotel. THELEELA has a strong visible pipeline of ~1,008 hotel keys, including BKC. Alongside, it has 38 keys under development at Udaipur, 19 keys at Coorg and ~245 branded residences across Dubai and Mumbai, providing clear mediumterm growth visibility and reinforcing into a globally scaled hospitality platform

Capital Structure Reset Powers the Next Growth Cycle

THELEELA is following a hybrid growth strategy, retaining and expanding its owned portfolio while adding keys through capital - light management contracts, supporting disciplined capital allocation. Post the INR 25 Bn IPO, in June 2025, the company reduced its debt by ~INR 23 Bn, lowering net debt/EBITDA from 6.1x to 2.3x. Concurrently, interest costs were reduced through renegotiation of term loans. The balance - sheet deleveraging has significantly lowered financing outflows and improved capital allocation flexibility. The company is expected to generate cumulative operating cash flow of ~INR 34 Bn over FY26E–FY29E, and to fund majority of its ~INR 35 Bn investment over the next 3 - 4 years through internal accruals

Optionality - THELEELA has introduced ‘ARQ’, a by-invitation ultra - luxury club, expected to boost revenue by adding INR 1,000 Mn every year.

Investment View: We initiate coverage on THE LEELA with a BUY rating and an FY28E EV/Adj. EBITDA of 18.0x to arrive at a TP of INR 510, implying an upside potential of 22.3%.. We expect Revenue and EBITDA to expand at a CAGR of 16.9% and 18.2% respectively over FY26E–29E

Key Risks: Extended geopolitical conflict, luxury market ARR risk and execution risk.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

.jpg)