2025-10-14 03:06:55 pm | Source: Motilal Oswal Financial Services Ltd

Buy KPIT Ltd For Target Rs. 1,500 by Motilal Oswal Financial Services Ltd

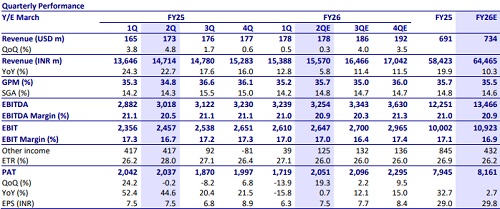

* KPIT may report flat QoQ CC growth due to lower contribution from Caresoft (2 months consolidation for 80% business vs. expectation of full consolidation).

* EBIT margins are expected to remain flat QoQ at 17%.

* Fixed-price deals are increasing, and some European deals are expected to ramp up.

* Commentary on Europe OEMs, budget allocation, the CV segment, and the China market will be key monitorable

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Disclaimer:

The content of this article is for informational purposes only and should not be considered financial or

investment advice. Investments in financial markets are subject to market risks, and past performance is

not indicative of future results. Readers are strongly advised to consult a licensed financial expert or

advisor for tailored advice before making any investment decisions. The data and information presented

in this article may not be accurate, comprehensive, or up-to-date. Readers should not rely solely on the

content of this article for any current or future financial references.

To Read Complete Disclaimer Click Here

Latest News

Gross NPAs of public sector banks fall to historic l...

Dwarikesh Sugar`s Q1 loss widens to Rs 26 crore, rev...

Hold R R Kabel Ltd For Target Rs. 2,596 - Prabhudas ...

Over 39.7 lakh rooftop solar systems installed under...

Accumulate Prudent Corporate Advisory Services Ltd F...

India`s gig internet workforce likely to triple to n...

Buy Mphasis Ltd For Target Rs.2,820 - Prabhudas Lil...

Evening Roundup : Daily Evening Report on Bullion, B...

Quote on IIP by Aditi Nayar, Chief Economist, ICRA Ltd

Quote on the latest IIP release by Vikrant Chaturved...

More News

Financials Banking Sector Update : Reconciling banking business updates with systemic data b...

Healthcare Monthly Sector Update : Acute/Chronic witness highest YoY growth in 24m By Motilal Oswal Financial Services Ltd

Financials Banking Sector Update : Are there upside risks to FY27E credit growth by Motilal Oswal Financial Services Ltd

Consumer Sector Update : Earnings outlook materially improves for the sector by Motilal Oswal Financial Services Ltd