Buy KEC International Ltd For Target Rs. 915 By JM Financial Services

Weak quarter; on a strong growth trajectory

KEC International (KEC) reported weak earnings in 2Q26 as PAT at INR 1.6bn was below JMFe/ consensus of INR 1.8bn due to higher interest and depreciation. While execution was strong in 2Q led by T&D, debt rose to record highs of INR 65bn amid rise in NWC levels. NWC rose QoQ to 138 days in Sept-25 due to delay in JJM payments, back ended payments in metro projects and payment spillover in Afghanistan projects. KEC expects NWC to normalize by Mar-26. Factoring in 1H26, we have lowered other income and increased interest cost estimates leading to EPS cuts of 8%/2% in FY26/27E. Backed by recovery in margins from a cyclical bottom, we expect robust 42% EPS CAGR over FY25-28E. Further, after the recent correction in stock, KEC is currently trading attractively at 15x/12x FY27/28E EPS. Hence, we upgrade the stock from HOLD to BUY with a revised price target of INR 915 (17x Sept-27 EPS).

* Earnings below JMFe due to higher interest and depreciation expenses: Consolidated revenue grew by 19% YoY to INR 61bn (JMFe: INR 59bn) led by 44% growth in T&D revenue to INR 40.8bn while non-T&D revenue declined by 12% YoY. EBITDA grew by INR 34% YoY to INR 4.3bn (in-line) while EBITDA margin expanded by 80bps YoY to 7.1% (JMFe: 7.3%). Standalone EBITDA margin at 6.2% (+110bps YoY) was below consolidated margins of 7.1% due to margin erosion in legacy ME projects and profit capture in Dubai/ME fabrication business in subsidiary. Other income declined sharply by 30% YoY to INR 46mn (JMFe: INR 100mn). Interest costs grew by 2% YoY/14% QoQ to INR 1.72bn (2.8% of sales) due to higher debt levels. PAT at INR 1.6bn was below JMFe of INR 1.8bn due to higher interest and depreciation expenses.

* NWC and debt levels rise in 2Q: KEC’s NWC increased QoQ from 128 days in Jun-25 to 138 days in Sept-25 due to delay in JJM payments, spillover in Afghanistan projects and back ended payments in the metro projects. KEC expects NWC to normalize by Mar-26 led by improved recoveries from JJM projects, Afghanistan payments (c.INR 2.7bn) and release of payments from completed metro projects. Net debt + acceptances rose sharply by INR 11bn QoQ/INR 12bn YoY to record highs of INR 64.8bn due to increased execution and rise in NWC. KEC’s JJM order backlog stood at INR 16bn as of Sept-25 dominated by Orissa (INR 10bn) and MP (INR 6bn). Outstanding debtors in the water vertical stand at c.INR 8.75bn.

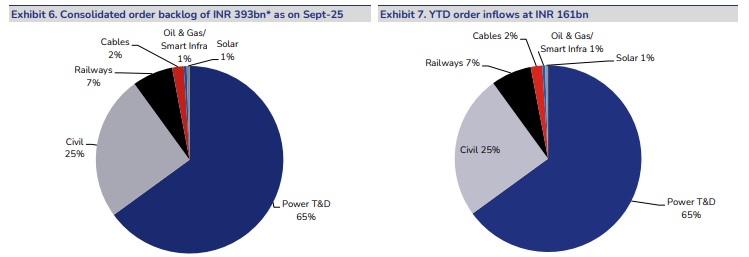

* Maintains FY26 revenue and order inflow guidance; bid pipeline robust at INR 1.8tn: With strong order inflows of INR 161bn in YTD, KEC’s order backlog stood at INR 393bn (1.7x TTM revenues) as of Sept-25. Additionally, KEC is also L1 in orders of INR 50bn+ (largely T&D). With a robust bid pipeline of INR 1.8tn dominated by T&D (c.INR 650bn) & Civil (c.INR 600bn), KEC is confident of achieving inflows of INR 300bn for FY26E. KEC has maintained its FY26 revenue growth guidance of 15% with EBITDA margins of 8% (earlier: 8-8.5%).

* Upgrade to BUY: We like KEC given its diversified capabilities, huge opportunity potential, industry leading return ratios and strong parentage. EBITDA margins have been impacted due to few legacy projects and losses in Railways vertical. Factoring in 1H26 performance, we have lowered other income and increased interest cost estimates leading to EPS cuts of 8%/2% in FY26/27E. Backed by recovery in margins from a cyclical bottom, we expect robust 42% EPS CAGR over FY25-28E. Further, after the recent correction in the stock, KEC is currently trading attractively at 15x/12x FY27/28E EPS. Hence, we upgrade the stock from HOLD to BUY with a revised price target of INR 915 (17x Sept-27 EPS).

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361