Buy HDFC Bank Ltd For Target Rs.976 By Elara Capital

Steady quarter, valuations reassuring

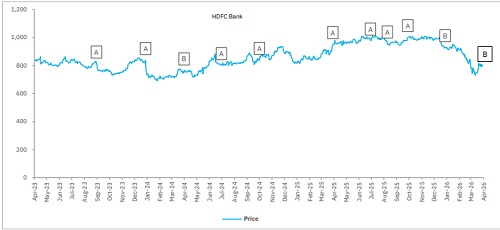

HDFC Bank’s (HDFCB IN) Q4FY26 PAT of INR 192bn (up 9% YoY) was marginally above estimates, led by higher trading gains, lower opex and curtailed credit costs (35bps), even as NII was marginally below estimates. Q4FY26 saw better loan growth outcomes (up 12.1% YoY/4.1% QoQ), with the bank confident of sustaining the momentum. We have been highlighting HDFCB’s conundrum to manage growth versus NIM versus LCR versus CD ratio outcomes, which may cause challenges. An upswing in core earnings seems still some time away. With the recent developments at the bank, we remain watchful of trends on softer aspects, which will continue to be an overhang. However, a correction in multiples, and higher discount versus peers render risk-reward favorable with limited downside. Nevertheless, a rerating may take time given limited near-term triggers. So, we prune our target price to INR 976 (earlier INR 1,147) but maintain BUY, drawing comfort on valuations.

Improving growth momentum; but certain monitorables persist: FY26 saw an improvement in loan growth. HDFCB reported ~12% YoY growth, with deposit growth at >14% YoY (partly supported by year-end dynamics), leading to an improvement in the CD ratio. Per management, the CD ratio is unlikely to be a binding constraint on growth, with regulatory comfort also supporting this stance. So, expect loan growth momentum to sustain. However, managing growth versus NIM versus LCR (now at 114%) versus CD ratio may cause certain dislocations. We see the risk of loan growth aspirations running short versus delivery, especially given sustained challenges on deposits (managing deposit growth, costs and improving incremental deposit market share could pose certain challenges).

Much to ponder on with focus on NIM trajectory: NIMs improved 2bps QoQ to 3.53% (on average earnings assets). While better system liquidity and deposit repricing may support NIM, deposit needs in FY27 may call for stickier costs that may strain NIMs. Given low credit cost, operating levers from opex and improved fee income will be key to earnings trajectory.

Asset quality benign: Slippages were curtailed (0.9% versus 1.2% QoQ), with steady progress across segments. The bank seems confident of no major red flags and curtailed credit costs outcomes. It carries a total (floating and contingent) buffer of 1.2% of loans, which renders comfort. We see steady credit cost outcomes for the bank.

Maintain Buy with a lower TP of INR 976: A merger of this scale is an onerous ask, but HDFCB is managing this well. The past two years have been challenging, with transition on both sides of the balance sheets. And the recent episodes have hit valuations (~14% underperformance in past two months) implying that the bank trades at 1.5x FY26E P/BV and at a significant discount to ICICI Bank now. A valuation re-rating could take time with limited near-term trigger, but we also find limited downside here given RoA/RoE potential of 1.8-1.9%/14-15%. We thus maintain BUY with lower SoTP-TP of INR 976 (earlier INR 1,147). Key monitorables hereon will be certain softer aspects. Our FY27/FY28 earnings estimates broadly remain unchanged and we introduce FY29 earnings estimates.

Please refer disclaimer at Report

SEBI Registration number is INH000000933