Buy HDFC AMC Ltd for the Target Rs. 3,200 by Emkay Global Financial Services Ltd

HDFC AMC delivered a decent performance in Q4FY26. QAAUM at Rs9.3trn was largely flat sequentially despite market volatility, with overall QAAUM market share maintained at 11.4%. Revenue at Rs10.5bn declined 2.2% QoQ, resulting in revenue yield at 46bps. EBITDA margin at 80.4% was down 140bps QoQ, driving down EBITDA, at Rs8.5bn (-2% QoQ). PAT at Rs6.2bn was down 19% QoQ, largely owing to lower other income. While the existing book is likely to see a 3-4bps hit given the implementation of the new base TER regulations, the management plans to largely offset this through optimization of commissions and prudent management of other costs. On baking in Q4 developments, our revenue estimates are largely unchanged, while we cut PAT estimates by ~1% over FY27-28. Given its strong brand, distribution strength, and healthy investment performance, HDFCAMC is poised to deliver healthy AUM compounding and top-tier profitability, in our view. We maintain BUY and Mar-27E TP of Rs3,200, implying FY28E P/E of 37x.

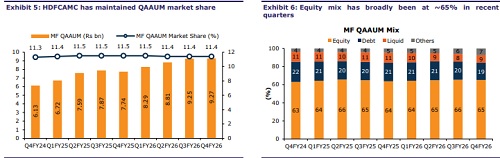

AUM remains largely flat QoQ; yields largely stable

HDFCAMC’s QAAUM at Rs9.3trn was largely flat QoQ, despite market volatility. While equity AUM was largely flat QoQ, the AMC saw strong sequential growth in the passives segment. During Q4FY26, revenue yields at 46bps were largely stable QoQ, driving revenue at Rs10.5bn (-2.2% QoQ), largely in line with our estimate of Rs10.6bn. EBITDA margin at 80.4% contracted by 140bps QoQ, largely on account of higher employee costs and other expenses. Core PAT (ex-other income) at Rs6.1bn declined 5.4% QoQ, mainly due to a ~4% QoQ decline in EBITDA and higher depreciation. PAT at Rs6.2bn declined 19% QoQ and was ~8% lower than our estimate, owing to lower other income.

Regulatory impact manageable; long-term mindset among investors

With respect to the regulatory change in base TERs, the management mentioned that the existing book is likely to see a gross impact of 3-4bps. However, this will be largely offset by optimizing commission payouts and other costs. The management highlighted that MF investors have displayed matured behavior while maintaining a long-term mindset despite volatility in equity markets. While HDFCAMC maintained its QAAUM market share at 11.4% in Q4, its unique investors at 16.7bn increased at a 36% CAGR over Q4FY23-Q4FY26, with market share expanding QoQ to ~27%. Further, a large part of the growth in unique investors was driven by fintech channels.

We maintain BUY and Mar-27E TP of Rs3,200

To reflect Q4 developments, we tweak our estimates which results in largely unchanged AUM and revenue estimates over FY27-28. However, we cut our PAT estimates by ~1% over FY27-28 and introduce FY29 estimates. Given its strong brand and retail franchise, distribution strength, and consistent investment performance, HDFCAMC is poised to deliver healthy AUM compounding and top-tier profitability, in our view. We maintain BUY and Mar-27E TP of Rs3,200, implying FY28E P/E of 37x.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354