Buy Emami Ltd For Target Rs. 725 by Motilal Oswal Financial Services Ltd

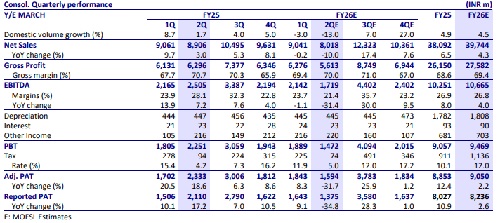

* 2Q demand was hit by the extended monsoon. Revenue to fall 10%, led by a 13% domestic volume decline.

* Summer portfolio (talcum powder and cooling hair oil) are significantly impacted by poor summer and continued monsoon, in addition to a strong base.

* GM is expected to contract by 70bp YoY. EBITDA is likely to decline 670bp YoY on negative operating leverage.

* The company is focusing on LUPs targeting middle-income consumers, which contribute ~20% of its revenue.

* Performance of D2C brands like The Man Company and Brillare will be a key monitorable.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Cement Sector Update : Earnings downgrade behind; cost reversal to begin from exit-2Q by Mot...