Buy Canara Bank Ltd For Target Rs.115 by Motilal Oswal Financial Services Ltd

NII misses estimate; other income drives earnings

Asset quality improves

* Canara Bank (CBK) reported 3QFY25 standalone PAT at INR41b (12.3% YoY growth, in line) because of higher other income, partly offset by lower NII and higher provisions.

* NII declined 2.9% YoY to INR91.5b (5% miss). NIM moderated 15bp QoQ to 2.71% during the quarter.

* The loan book grew 11.2% YoY/4% QoQ to INR10.2t, while deposit growth was modest at 8.4% YoY/1.6% QoQ to INR13.7t. CASA ratio moderated to ~30% in 3QFY25. Management guided 10% credit growth for FY25.

* On the asset quality front, total slippages stood at INR24.6b (INR23.5b in 2QFY25). Healthy recovery and write-offs led to 39bp/10bp QoQ improvement in GNPA/NNPA to 3.34%/0.89%. PCR was stable at 74.1%.

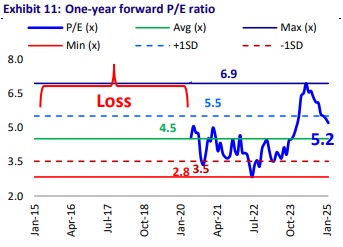

* We broadly maintain our projections and estimate CBK to deliver FY26E RoA/ RoE of 1%/17.7%. We reiterate our BUY rating with a TP of INR115 (premised on 0.9x Sep’26E ABV).

Deposit growth modest; NIM moderates 15bp QoQ

* CBK reported 3QFY25 standalone PAT at INR41b (12.3% YoY growth, in line) amid better other income while NII misses estimates. During 9MFY25, earnings grew 11.4% YoY to INR120.2b (4QFY25E at INR40.1b; implying 6.8% YoY growth).

* NII declined 2.9% YoY to INR91.5b (5% miss). NIM moderated 15bp QoQ to 2.71%. Other income grew 16.5% QoQ to INR58b (35.1% YoY, 20% beat). Treasury income stood at INR9.45b vs. INR6.61b in 2QFY25. Total revenue thus grew 9% YoY (4% beat).

* Operating expenses grew 3% YoY to INR71.1b (up 7.1% QoQ, in line). The C/I ratio thus rose 112bp QoQ to 47.6%. Provisions came in at INR23.9b (26% YoY/ 6.5% QoQ, 14% higher than MOFSLe). PPoP grew 15.2% YoY to INR 78.4b (4% beat).

* The loan book grew 11.2% YoY/4% QoQ, led by the retail segment, which grew 7% QoQ. Deposit growth was modest at 8.4% YoY (1.6% QoQ), led by term deposits. CASA ratio thus moderated by 127bp QoQ to ~30%. The domestic CD ratio stood at 76.6%, and the bank is comfortable with ~78%.

* GNPA/NNPA ratios improved 39bp/10bp QoQ to 3.34%/0.89%. PCR was stable at 74.1%. Total slippages stood at INR24.6b (INR23.5b in 2QFY25). Credit costs were 0.89% vs. FY25 guidance of 1.1%.

* The total SMA Book moderated to 1.14% in 3QFY25 from 1.48% in 2QFY25, due to a reduction in the SMA-2 book.

Highlights from the management commentary

* Management expects INR5-6b of recovery in 4Q. The recovery would be led by two accounts.

* Management guided 9% YoY deposit growth for FY25.

* LCR stood at 123%, and due to the draft LCR guidelines, it can come down to 110- 111%. For this, the bank has started offering new TDs for long-term deposits of longer maturities. This will help negate the drag on the LCR to 115-120%.

* Slippages break up: Agri - INR8b, Retail - INR5b, MSME was INR10b. All these total to INR23b. No corporate account slipped to the NPA.

Valuation and view

CBK reported a mixed quarter with inline earnings as higher other income offsets the higher provisions and tepid NII as NIMs moderated 15bp sequentially. Loan growth was led by the retail segment, while deposit growth was modest with the CASA ratio moderating sequentially. There has been an improvement in overall asset quality ratios, with higher recoveries and upgrades and lower slippages. Management expects credit costs to be ~1.1% for FY25. SMA book and credit costs also were controlled during the quarter. We broadly maintain our projections and estimate CBK to deliver FY26E RoA/ RoE of 0.99%/17.7%. Reiterate BUY with a TP of INR115 (premised on 0.9x Sep’26E ABV).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412