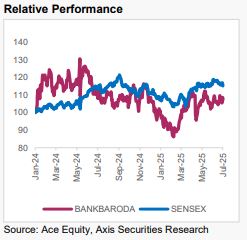

Buy Bank of Baroda Ltd For Target Rs.275 by Axis Securities Ltd

NIMs Better Managed vs. Peers; BUY Stays on Reasonable Valuations! Est. Vs. Actual for Q1FY26: NII – BEAT; PPOP – BEAT; PAT – BEAT Changes in Estimates post Q1FY26 FY26E/FY27E (in %): NII: -1.5/-0.1; PPOP: -2.5/-5.4; PAT: -0.7/-1.0

Recommendation Rationale

- Near-Term Pressure On Margins to Continue; Recovery Expected in H2: BoB’s managed margin compression better (at 7 bps QoQ) than most peers, who have reported a sharper NIM decline. With the Jun’25 repo rate cut reflecting in Q2, NIMs are set to contract further. Currently, 35% of the portfolio is EBLR-linked, 45% is MCLR-linked, 6% is fixed rate, and the balance 14% is linked to G-Sec and T-bills. While the EBLR loans will reprice downwards immediately, the pass-through on the MCLR loans will be with a lag. The rate action taken by the bank on deposits will start reflecting in the CoD/CoF from Q3 onwards, with ~70-80% of the deposits getting repriced. The overall benefit of CoD is expected to be 15-17 bps. Thus, the management has guided NIMs to be maintained between 2.85-3% in FY26E. We expect BoB to maintain NIMs between 2.8-2.9% over FY26-28E.

- Growth to be Led by RAM; Corporate Growth Soft: The management has continued to guide the pace of credit growth to range between 11-13% for FY26, with the corporate portfolio growing at ~9-10%. The growth opportunities in the highly rated corporates continue to remain subdued, with pricing pressures persisting and most of these corporates tapping bond markets, citing better rates. Hereon, focus will remain on the RAM segment as the bank aspires to improve its mix in the portfolio to 64-65% over the medium term vs 56% currently. With BoB’s LDR at 84.1%, we see limited scope for meaningful credit growth improvement. We pencil-in credit growth of 12% CAGR over FY25-28E, with deposit growth keeping pace, enabling BoB to maintain a steady LDR.

- Asset Quality Outlook Not Concerning: The slippages in Q1FY26 were higher owing to a large international account and a slight increase in slippages from the legacy PL portfolio. Against the international accounts, the bank has made a prudent provision of 40%. However, the management expects resolution/recovery in this account during FY26. Apart from this account, the international portfolio continues to behave well. In the domestic portfolio, the PL slippages continue to remain within the threshold of the bank. The increase in SMA1 and 2 inched up marginally to 0.4% vs 0.33% QoQ, owing to two government-guaranteed accounts. We do not foresee any major challenges to asset quality and thus expect credit costs to remain under control at 0.6% (+/-5 bps).

Sector Outlook: Positive

Company Outlook: BoB has been able to maintain NIMs better than its PSU peers. However, nearterm challenges on NIMs will persist before an anticipated recovery from H2 onwards. A sharperthan-expected NIM contraction poses risks to the 1% RoA delivery. The bank is making conscious efforts to strengthen the fee income profile. Opex growth is expected to be controlled, marginally below business growth. With no major asset quality challenges in sight, credit costs are expected to remain under control. We expect RoA/RoE delivery of 0.95-1%/12-13% over FY26-28E, with adverse NIM impact being a key downside risk to the ~1% RoA delivery. We expect BoB to deliver an Advances/Deposits/NII/Earnings growth of 12/12/11/6% CAGR growth over FY25-28E. Current Valuation: 0.9x FY27E ABV; Earlier Valuation: 0.9x FY27E ABV Current TP: Rs 275/share; Earlier TP: Rs 280/share Recommendation: We maintain our BUY recommendation on the stock based on reasonable valuations. Alternative BUY Ideas from our Coverage: HDFC Bank (TP – Rs 2,300); ICICI Bank (TP – Rs 1,650)

Financial Performance

- Operational Performance: BoB’s advances grew by 13/-2% YoY/QoQ, led by Retail advances, which grew by 18/2% YoY/QoQ (26% Mix vs 25% QoQ). Deposit growth was lower than credit growth and stood at 9/-2.5% YoY/QoQ. Domestic deposits grew by 9/-3% YoY/QoQ. Domestic CASA deposits grew by 5/-5% YoY/QoQ. CASA Ratio declined to 39.3% vs 40% QoQ. C-D Ratio (net) stood at 82.7% vs 82.2% QoQ. International deposits grew by 15/1% YoY/QoQ.

- Financial Performance: NII growth slowed down and was flattish (-1% YoY) and grew by 4% QoQ. NIMs contracted by 7 bps QoQ and stood at 2.91% vs 2.98% QoQ (restated, Q4 reported NIMs stood at 2.86%). Non-interest income growth was strong at 88% YoY and decreased by 10% QoQ. Treasury gains supported non-interest income growth (at Rs 22.3 Bn vs Rs 15.6 Bn QoQ). Fee income (0.5% of avg total loans) grew by 10% YoY. Opex growth was controlled at 14/-3% YoY/QoQ, led by a sequential decline in both Employee (-1% QoQ) and other Opex (-5% QoQ). C-I Ratio stood at 48.9% vs 49.2/49.9% YoY/QoQ. PPOP grew by 15/1% YoY/QoQ. Credit costs stood at 78 bps vs 62 bps QoQ. PAT grew by 2% YoY and de-grew by 10% QoQ.

- Asset Quality remained broadly stable with GNPA/NNPA up by 2 bps each to 2.28/0.6% vs 2.26/0.58% QoQ. Slippages during the quarter were higher QoQ, with the slippage ratio at 1.1% vs 1% QoQ. PCR was steady at 74% vs 75% QoQ.

Outlook

We believe there is limited room for LDR improvement (given the bank operates at ~82-83%), and the scope to accelerate growth is also limited. Thus, deposit growth will have to keep pace with credit growth. While the bank has fared better vs its peers in terms of margins, near-term pressures on NIMs will be visible. An unfavourable (sharper than expected) outcome on NIM would weigh on the RoA of the bank. We trim our NII estimates by 1-2% over FY26-27E and broadly maintain our earnings estimates with minor tweaks. Currently, we expect BoB to deliver Credit/Deposit/NII/Earnings growth of 12/12/11/6% CAGR over FY25-28E, while continuing to deliver RoA/RoE of ~0.95- 1%/12-13% over FY25-28E.

Valuation & Recommendation

We believe current valuations at 0.8x FY27E are reasonable for a sustained RoA delivery of 0.95-1%. However, NIM performance and growth resuming would be key drivers for stock performance. We value the stock at 0.9x FY27E ABV to arrive at a target price of Rs 275/share, implying an upside of 13% from the CMP. We maintain our BUY recommendation on the stock.

Key Risks to Our Estimates and TP

• The slowdown in systemic credit growth would impact our estimates. • Asset quality concerns could result in elevated credit costs, thereby impacting our earnings estimates.

For More Axis Securities Disclaimer https://simplehai.axisdirect.in/disclaimer-home SEBI Registration number is INZ000161633

Tag News

India`s outward FDI rebounds strongly since COVID defying global trend