Buy Bandhan Bank Ltd For Target Rs. 210 Motilal Oswal Financial services Ltd.

NII in line; lower provisions drive earnings

Slippages, SMA pool declining steadily

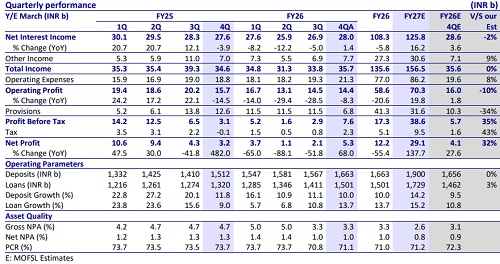

* Bandhan Bank reported 4QFY26 PAT of INR5.3b (up 68% YoY, 32% beat). NII grew 4% QoQ to INR27.9b (in line).

* Margin improved by 30bp QoQ to 6.2%, aided by a reduction in CoF (down 20bp QoQ) and improvement in yields (up 10bp QoQ).

* Net advances grew by 13.7% YoY (up 6.4% QoQ). Deposits grew by 10% YoY/6.1% QoQ. CD ratio increased marginally to 90%.

* Fresh slippages declined to INR10.3b from INR13.1b in 3QFY26. GNPA ratio improved 6bp QoQ to 3.27%, while NNPA improved 2bp QoQ to 0.97%. PCR ratio was broadly stable at 71.1%.

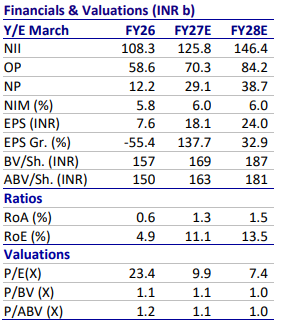

* We had upgraded Bandhan in 3QFY26 on the back of improving visibility on growth and improvement in asset quality. We estimate Bandhan to deliver RoA of 1.3%/1.5% in FY27E/FY28E. Maintain Buy with a revised TP of INR210 (1.2x Sep’27E ABV).

Margin improves 30bp QoQ; guides FY27-exit RoA at 1.6-1.7%

* 4Q PAT stood at INR5.34b (up 68% YoY, 32% beat), driven by lower credit costs and 30bp QoQ improvement in NIM.

* NII grew to INR27.9b (4% QoQ) as NIMs improved 30bp QoQ to 6.2%, aided by 20bp decline in CoF and 10bp improvement in yields. Management guides for further 10-20bp NIM expansion over the next 2- 3 quarters amid TD repricing.

* Other income grew 10% YoY/12% QoQ to INR7.7b (9% beat), supported by strong fee income (processing, TPP and product/service charges).

* Opex jumped 10% QoQ to INR21.25b (8% above MOFSLe), largely attributable to two non-recurring items: PSL-related costs and IT/ technology expenses totaling INR1.2b. C/I ratio increased to 59.6%.

* Gross advances grew 13% YoY/6% QoQ to INR1.5t. Non-EEB book grew 25% YoY/5% QoQ and now constitute ~65% of advances. EEB book grew 8% QoQ and collection efficiency improved (99.3%). Secured mix increased to 56.2%.

* Deposits grew 10% YoY/6.1% QoQ to INR1.66t, with CASA ratio improving 204bp QoQ to 29.3%, driven by strong CA growth. CASA + Retail deposits now form 72% of total deposits.

* GNPA ratio improved by 6bp QoQ at 3.27%, while NNPA improved to 0.97%. PCR stood at 71.1%. Fresh slippages declined sharply to INR10.28b (down ~22% QoQ), with improvement led by EEB segment. Credit cost declined significantly to 2.0% (vs 3.3% in 3Q).

Highlights from the management commentary

* ROA guidance: Management reiterated FY27-exit ROA target of 1.6-1.7%, led by further credit cost reduction, NIM expansion, higher other income, and lower PSL costs. Sequential improvement is expected from the 4Q level of 1.1%.

* 4Q LCR was 131% (periodic), with average LCR range of 130-148% during the quarter. The reduction in bulk deposits has helped to reduce LCR volatility.

* ECL transition impact is estimated at INR12.5b (based on Dec’25 portfolio), to be spread over five years (INR2.5b/year), resulting in a 16-17bp per year impact on CRAR.

* Management expects a further 10-20bp NIM improvement over the next 2-3 quarters, as term deposits continue to reprice lower on renewal. The FY27-exit NIM guidance is 6.5% on earning assets (6% on total assets).

Valuation and view

* Bandhan reported a strong quarter, led by a 30bp QoQ expansion in NIMs and a strong improvement in credit costs to 2% (vs. 3.3% in 3Q). Business momentum was also robust, supported by the seasonally strong 4Q. Management expects loan growth to remain healthy at 14-15%, with advances likely to grow in line with or ahead of overall business growth. NIMs improved to 6.2%, and are guided to expand further by 10-20bp over the next 2-3 quarters, aided by repricing of term deposits. The bank has indicated an exit FY27 NIM guidance of ~6.5% on earning assets (~6% on total assets), while we conservatively factor in ~6% NIM on earning assets. On asset quality, we expect improving forward flows for both the industry and Bandhan, particularly in the MFI segment, which should lower credit costs to ~1.9% in FY27E (vs. 3.2% in FY26).

* We had upgraded Bandhan in 3QFY26 on the back of improving visibility on growth and lower credit cost. We upgrade our earnings estimates by 4-5% for FY27/FY28 and expect Bandhan to deliver RoA of 1.3%/1.5% in FY27E/FY28E vs. 0.6% in FY26. Maintain BUY with a revised TP of INR210 (1.2x Sep’27E ABV)

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

Tag News

Trade Idea of The Day - State Bank of India Target Rs. 28 - Religare Broking Ltd