Buy Adani Ports & SEZ Ltd for the Target Rs.1,820 by Motilal Oswal Financial Services Ltd

India’s port volumes to be hit; APSEZ better placed

* The disruption at the Strait of Hormuz has caused a setback in global shipping, leading to slower cargo movement and rerouting. Indian ports are facing challenges such as unscheduled cargo inflows from diverted vessels, resulting in congestion and export backlogs. This disruption is particularly significant given India’s heavy dependence on crude imports.

* While major ports handle a significant share of this trade, APSEZ’s exposure remains relatively limited, with liquid cargo accounting for less than 10% of total volumes. Within this category, crude oil handling accounted for ~6% in FY25, moderating to ~5% in 9MFY26, while gas volumes continue to represent a small portion of the mix at ~2% in both periods. Consequently, the overall impact on APSEZ is expected to remain contained. Further, the addition of NQXT port volumes is likely to ensure robust overall volumes going forward.

* All-India major port volumes grew 3.5% YoY in Feb’26 and ~8% YTD in FY26, fueled by healthy traction in petroleum, containers, and coking coal (albeit from a low base). Non-major port volumes inched up ~3% YoY, led by steady traction in container traffic (+5% YoY), while petroleum, oil, and lubricants (POL) volumes remained largely flat YoY.

* APSEZ reported ~14% and ~11% volume growth in 4QFY26 until Feb’26 and 9MFY26, respectively, primarily driven by robust container throughput, which grew ~20% YTD until Feb’26. Coal volumes remained subdued over the past few quarters due to weak industry demand for imported coal and disruptions at Tata Power’s Mundra plant. However, the impact on profitability was largely mitigated through take-or-pay contracts on coal cargo, supporting stable EBITDA despite lower volumes.

* With improving earnings visibility and limited downside risk from ongoing geopolitical tensions, APSEZ is well-positioned to sustain growth, aided by diversified port volumes, the acquisition of NQXT, and the expansion of integrated end-to-end logistics offerings. This strategy is driving higher customer wallet share and enhancing cargo stickiness, while its scalable and diversified model underpins long-term growth. These factors reinforce APSEZ’s ambition to become India’s largest integrated transport utility by 2029, with logistics and marine emerging as key growth engines alongside its core ports business. We reiterate our BUY rating with a TP of INR1,820 (based on 15x FY28E EV/EBITDA).

Scale leadership and rising market share underpin long-term growth outlook

* APSEZ operates the largest private port network in India, with 15 ports and terminals across the west, south, and east coasts. The network offers a total capacity of 637mmt; it also has four international ports in Israel, Sri Lanka, Tanzania, and Australia.

* The company has commissioned the Haldia bulk terminal in Mar’26, with a capacity of ~4MTPA and a draft of 8.5m, supported by a dedicated rail line and integrated conveyor system.

* APSEZ’s domestic market share stood at 26.4% as of Dec’25. Management highlighted that its domestic port volume growth over the past decade has been nearly three times the industry growth rate.

* The container market share has also expanded steadily to 45.8% from 36% during Mar’20-Dec’25. Key capacity expansions, such as the automated Colombo West International Terminal and new berths at Dhamra, along with the rapid ramp-up of Vizhinjam, are strengthening APSEZ’s growth pipeline.

* Looking forward, management retains its target of 850mmt of domestic and 150mmt of international cargo volumes by 2030, with deeper integration into DFC-linked hinterland corridors and industrial clusters driving long-term growth.

Logistics business – Accelerating the shift to a unified logistics ecosystem

* As APSEZ aims to become India's largest integrated transport utility company by 2029, it is strengthening its capabilities across all logistics segments (ports, CTO, warehousing, last-mile delivery, ICDs, etc.). This enables the company to offer end-to-end services, capture a higher wallet share, and ensure cargo volumes remain sticky.

* Adani Logistics Limited (ALL) has expanded its services to cover container train operations, container handling in logistics parks, and warehouses, offering storage and trucking solutions. With 12 multi-modal logistics parks, 132 trains, 3.1m sq. ft. of warehousing space, and 1.3mmt of grain silos, ALL aims to establish a nationwide presence by further developing logistics parks and warehouses.

* With significant capital investments planned for trucking operations—INR10-15b in FY26 and INR50b by FY30—APSEZ maintains a hybrid model, owning 937 trucks and operating over 26,000 via third parties. It is also expanding valueadded services like freight forwarding to improve RoCE.

Marine services: A swiftly scaling, high-margin growth engine

* Marine operations have emerged as another high-growth vertical within APSEZ, with a diversified fleet of 127 vessels (excluding 46 vessels operated by Adani Harbor across the APSEZ ports), including tugs, anchor-handling tug supply vessels, multipurpose support vessels, workboats, and barges.

* The business has been strengthened by acquisitions such as Ocean Sparkle in 2022 and Astro Offshore in 2024, along with the establishment of TAHID to manage international operations in the MEASA region.

* In 3QFY26, marine revenue jumped 91% YoY to INR7.7b, with EBITDA surging to ~INR4.3b and margins expanding to 55.3%. The surge was driven by vessel additions, integration of acquired entities, and higher demand from Tier-1 customers.

* The marine business’s RoCE improved to 15% in 1HFY26 from 13% in FY25.

* Management is aiming to double its revenue from INR11.4b in FY25 (INR19.6b achieved in 9MFY26), positioning the segment as a profitable and capitalefficient business that complements port operations while extending APSEZ’s reach across global shipping routes.

Valuation and view

* With strong cash flows, a healthy cash balance of INR118b, and a net debt-toEBITDA ratio of 1.9x, APSEZ is well-positioned for further expansion. Capacity enhancements at key ports, ongoing infrastructure projects, and global port acquisitions provide clear visibility for steady growth in FY26 and beyond.

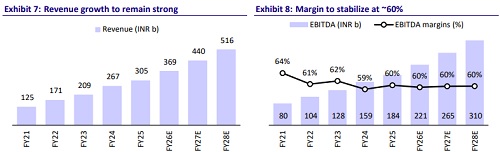

* APSEZ’s diversified cargo mix and ongoing infrastructure investments are expected to support its volume growth. We anticipate APSEZ to report an 11% growth in cargo volumes over FY25-28. This growth is likely to drive a CAGR of 19%/19%/23% in revenue/EBITDA/PAT over FY25-28E. We reiterate our BUY rating on the stock with a TP of INR1,820 (premised on 15x FY28E EV/EBITDA).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041