Buy ACME Solar Ltd for the Target Rs.350 by HSBC

* One of India’s fastest-growing, vertically-integrated, independent power producers of renewable energy

*c6GW contracted capacity gives long-term earnings visibility; FDRE projects and BESS to improve returns

* Initiate with a Buy (TP INR350); we forecast an EBITDA CAGR of 72% in FY26-28

Solar star. ACME Solar Holdings (ACME) is a fast-growing renewable energy independent power producer, which is fully vertically integrated in terms of engineering, procurement and construction, as well as operations and maintenance (O&M). ACME currently operates around 3GW of generation capacity and has c3.3GW contracted capacity under 25-year signed power purchase agreements (PPAs). These projects are anticipated to increase ACME’s overall capacity by 2.7x over the next 2-3 years. ACME also has a further 1.8GW of awarded projects that are still awaiting conversion into PPAs. Strategically, the business is evolving from a pure play solar provider to more complex firm and dispatchable renewable energy (FDRE) projects, which require a combination of solar, wind, and battery storage capacity.

Better with BESS. Renewable energy is already much cheaper than thermal power in India, and we believe renewables will get a further boost from BESS that captures energy from solar and wind that can be discharged later. The use of BESS enhances grid stability, reduces energy costs, and provides back-up power, especially during the evening peak period. As BESS costs fall and confidence around viability increases, we believe the adoption of renewables will increase. ACME already has 1.1GWH of BESS, which will allow it to generate additional merchant revenue before this capacity is integrated into more advanced FDRE projects.

Growth outlook. We forecast EBITDA to grow at a CAGR of 72% over FY26-28. Earnings visibility is strong as 84% of ACME’s contracted portfolio with 25-year fixed tariff PPAs are backed by central government agencies. We also think the company is well placed to benefit from the early adoption of BESS and FDRE projects. Working capital improved to 23 days from 93 days in FY24 due to a fall in receivables, which increases confidence in the strength of its balance sheet.

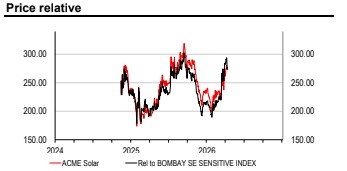

Valuation and risks. We value ACME on FY28 run-rate EBITDA, which is based on already-signed 25-year PPAs and those which we expect to be executed by end FY28. We assign a 10x EBITDA multiple, which reflects growth, in line with the average peer multiple for FY28. Adjusting for net debt as of March 2028, we derive an equity value of INR266bn. We discount it back to June 2026 (3M forward fair value, in line with our coverage) to arrive at a TP of INR350. Our TP implies c28% upside from current levels; accordingly, we initiate coverage on the stock with a Buy rating. Downside risks: (1) High leverage with projects financed with a 80-20 debt equity ratio, (2) rise in equipment and borrowing costs, (3) delay in commissioning of contracted capacity, and (4) lower-than-expected generation.

Above views are of the author and not of the website kindly read disclaimer