Add Bharat Forge Ltd For Target Rs. 1,480 By JM Financial Services

Beat on all fronts; domestic business to offset weakness in exports

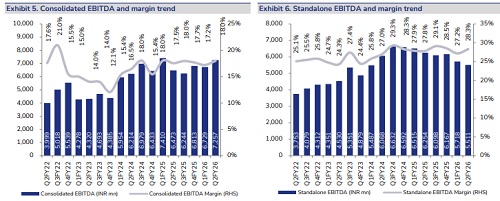

In 2QFY26, Bharat Forge’s (BHFC) consolidated EBITDA margin stood at 18% (+40bps YoY), 150bps above JMFe due to strong execution in defence and steady performance of overseas subsidiaries. Standalone EBITDA margin expanded 50bps YoY to 28.3% on account of cost reduction activities and favourable product mix. Tariff impact for the quarter stood at INR 240mn. The defence segment’s order pipeline remains robust at INR 95bn. While export momentum to the US is likely to remain subdued amid tariff overhang, the management expects ramp up of defence orders, domestic industrial business, and exports to non-US geographies to more than offset the weakness in the US. We raise our FY26E/27E EBITDA margin estimates by 109bps/91bps, translating into EPS increase by 10.9%/10.5%. We revise our rating from HOLD under the previous system to ADD under the new rating framework, with a TP of INR 1,480 at 35x (32x earlier) average FY27E/28E EPS. India-US trade deal to remain a key monitorable

* 2QFY26 – Consolidated margin above estimates: BHFC’s stand. net sales stood at INR c.19bn (-13% YoY, -8% QoQ). Total tonnage stood at c.56.4kt (-12% YoY, -9% QoQ). Realisation decreased by 2% YoY (+1% QoQ). Reported stand. EBITDA margin was 28.3% (+50bps YoY, +110bps QoQ). Consolidated revenue stood at INR 40bn (+9% YoY, +3% QoQ), 7% above JMFe. EBITDA margin stood at 18% (+40bps YoY, +80bps QoQ), 150bps above JMFe primarily due to strong execution in defence. Consol. EBITDA stood at INR 7.3bn (+12%YoY, +8% QoQ), 17% above JMFe. Consol. PAT stood at INR c. 3bn (+23% YoY, +5% QoQ), 5% above JMFe.

* Domestic business outlook: Domestic revenue declined 6% YoY (-2% QoQ) to ~INR 10bn in 2Q. CV revenue grew 1% YoY (-9% QoQ) to INR 2.4bn due to lower production volumes in anticipation of GST rate changes. The government’s capex push and an increase in construction and manufacturing activity remain medium-to-long-term growth drivers. PV revenue stood at INR 912mn (-1% YoY, -6% QoQ), owing to the consolidation of the gains seen over last year. The management expects steady performance to continue in medium-term, as vehicle demand is likely to be grow post GST rationalisation. Industrial segment revenue declined 7% YoY (+3% QoQ) to approximately INR 5.9bn. The sequential improvement in the segment was due to the execution of a defence order and good traction for heavy horse-power engines. BHFC has transferred all the defence dedicated assets of BHFC to its wholly owned subsidiary KSSL. BHFC’s defence order book stands at ~INR 95bn (domestic + exports) with additional domestic tender worth INR 14bn awaiting conversion. Further, it got defence business worth INR 2.5 bn for underwater systems, a key focus area for KSSL (to be executed in 1 year). The management expects to close more order wins for platforms/ projects they have participated in. Overall, BHFC expects to see a ramp-up in defence revenue, with full-year growth anticipated.

* Export business outlook – tariff headwinds to linger: Export revenue declined 20% YoY (-12% QoQ) to INR 9.4bn in 2QFY26. CV segment revenue stood at INR 2.8bn (-45% YoY, -37% QoQ), due to a combination of slow freight growth, weak sentiment and tariff uncertainty weighed on CV demand in North America. PV segment revenue, however, grew 7% YoY (+2% QoQ) to INR 2.95bn. Despite the demand challenges in the US, the YoY growth was primarily led by diversification efforts across geographies and products. Industrial revenue declined approximately 4% YoY (+8% QoQ) to INR 3.6bn, led by mixed performance across segments (construction mining/aerospace showed resilience, however, oil & gas was weak due to weak crude prices). Overall, the management expects 2H to be weak due to challenging demand condition in North America. The tariff impact for the quarter stood at INR 240mn

* Overseas manufacturing operations: During 2QFY26, overseas manufacturing subsidiaries revenue stood at ~INR 12.6bn (+11% YoY, -11% QoQ). EBITDA margin at EU operations declined 30bps YoY (+50bps QoQ) to 3.6%. BHFC’s review of its EU manufacturing footprint is on track. The US manufacturing operations reported an EBITDA margin contraction of 190bps QoQ to 4.2%. Additionally, the US Aluminium forging plant is ramping-up steadily, operating at 65% utilisation level.

* Other highlights: 1) BHFC’s standalone gross LT debt reduced QoQ to INR 8bn in 2QFY26 from 10.4bn in 1QFY26. The board has approved debt raise of up to INR 20bn towards organic and inorganic growth. 2) Capex guidance for FY26 stood at INR 5bn and the company is setting up a new dedicated forging and machining facility for aerospace. 3) AAM intergration is on track with consolidation of numbers started this quarter onwards.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361