Accumulate Oberoi Realty Ltd For Target Rs.1,820 by Prabhudas Liladhar Capital Ltd

Strong launch pipeline

Oberoi Realty Ltd (OBER) reported robust pre-sales growth of 96% YoY, along with 21% YoY collection growth in Q4FY26. OBER has demonstrated healthy growth momentum in pre-sales with ~9% CAGR over FY22-26, fuelled by successful new launches, rapid inventory absorption, and strong demand across the MMR market. We foresee 24% pre-sales CAGR over FY26-28E aided by new launches across Gurugram, Thane, Tardeo and Worli, and sustenance sales from their existing projects. Further, we expect annuity income to remain steady at Rs13-14bn, providing strong cash flow visibility. We retain our ‘Accumulate’ rating and DCF-derived NAV with SOTP-based TP of Rs1,820/share, implying 11% upside from current levels

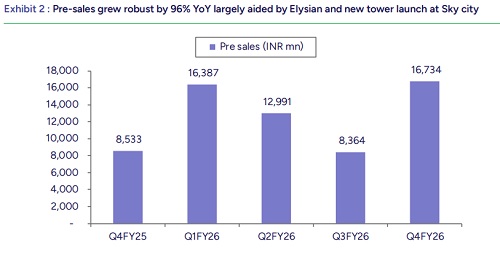

Robust sales growth largely aided by Elysian and sky city:

Operationally in Q4, OBER’s EBITDA increased 55% YoY to INR9.6bn; above our estimates, with EBITDA margin improving to 54.9%; up ~115bps YoY. For FY26, EBITDA stood at INR33.6bn, with 8% YoY growth and EBITDA margin at 55.9% (down ~280bps YoY). Consolidated revenues improved by 52% YoY at INR17.5bn largely aided by revenue bookings at Elysian and Sky city project. For FY26, revenues increased by 14% YoY to INR60.1bn. PAT increased by 62% YoY to INR7bn, while FY26, PAT increased 13% YoY to INR25.1bn.

Strong pre-sales & collections in Q4:

OBER’s pre-sales improved 96% YoY to INR16.7bn driven by new tower launch at sky city and sustenance sales especially from Elysian project. contributed INR 8.5bn and INR 3.2bn; respectively in Q4. 360 west contributed Rs1.3bn in Q4. For FY26, pre-sales grew 4% YoY to INR54.5bn. Average price realization stood at INR46,801psf (down 25% YoY) in Q4FY26. Leasing income increased 38% YoY and ~8% QoQ to INR3.1bn. Commerz III achieved occupancy of 98% in Q4 vs 90% in Q3 while Sky city achieved 72% occupancy in Q4 vs 56% in Q3. For FY26, reported leasing income of INR 11.3bn; up 46% YoY. Hospitality revenues improved to INR550mn, up 3% YoY. For FY26, it grew by ~3% YoY to INR 2bn. Collections stood at INR 9.3bn; up by ~21% YoY. However, it declined by 3% YoY to INR 42.5bn for FY26. Cash stands at Rs29.9bn; up by 6% QoQ.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271