Buy InterGlobe Aviation Ltd For Target Rs.5,600 by Motilal Oswal Financial Services Ltd

Volatile 4QFY26; stabilization expected in 1QFY27 Operating performance beats estimates

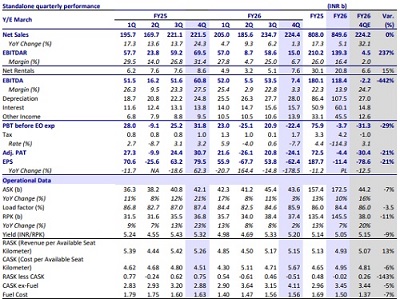

* InterGlobe Aviation (INDIGO) reported a 78% decline in EBITDAR to INR15b, led by higher forex loss (~INR48.8b), while EBITDA (ex-forex) was down only 5% YoY to INR56.3b. Despite the volatile 4Q impacting air travel and muted ASK growth YoY, INDIGO managed its costs better than expected. Hence, it significantly beat our EBITDA estimates (ex-forex loss) of INR48.7b.

* Due to continued capacity moderation following the Middle East airspace disruptions and network cancellations, the company guided a near-term ASK growth of ~3-4% YoY (1QFY27) as international operations gradually recover and redeployment of capacity takes place toward domestic and new metro airports. The Passenger Revenue per Available Seat Kilometer (PRASK) is expected to improve in the mid-teen range for 1QFY27, supported by better yields, higher load factors, and fuel surcharge implementation despite the ongoing seasonality and a low base from the 1QFY26 disruption (Operation Sindoor and the Air India aircraft crash).

* Factoring in better cost control by the company, we increase our FY27E/FY28E EBITDAR by 5%/2%. However, we largely retain our FY27E/FY28E earnings estimates. We value the stock at 9x FY28E EBITDAR to arrive at our TP of INR5,600. Reiterate BUY.

Highlights from the management commentary

* Aircraft ownership strategy: The company reiterated its accelerating aircraft ownership strategy as a key balance sheet optimization and long-term value creation lever, with total cash of INR516b (including INR362b free cash) enabling higher direct aircraft ownership. The company has prepaid loans on 17 aircraft in FY26. It currently owns 36 unencumbered aircraft worth over INR95b and 53 aircraft under finance lease structures. The company also announced a USD820m investment into its GIFT City entity for aviation asset acquisition. Management continues to view aircraft ownership as financially superior to idle cash due to better returns, lower financing costs, and reduced forex exposure over time.

* International operations and capacity deployment: The Middle East conflict led to the cancellation of ~160 daily flights, with international operations recovering from ~20% capacity initially to nearly two-thirds currently; full normalization is expected by end-Jun, while demand is set to improve in 2QFY27. Capacity is being redeployed to new metro airports and domestic leisure routes, with international and long-haul deployment remaining flexible and profit-driven.

* Fleet strategy: Pratt & Whitney's Aircraft on Ground (AOG) cases remain in the "40s," with expectations to reduce to the "30s" by the end of FY27. Fleet optimization efforts are focused on reducing damp leases and phasing out older aircraft, while OEM deliveries remain on schedule. In FY26, 72 aircraft were added, bringing the total fleet to 441. The induction of India’s first A321XLR has already supported early expansion into Europe, including Athens and Istanbul, with additional routes planned

Valuation and view

* Despite continued near-term headwinds from the Middle East airspace disruptions, elevated fuel costs, rupee depreciation, and higher damp-lease exposure, we remain confident in INDIGO’s growth strategy, anchored by India’s strong domestic demand base and steadily expanding international network.

* Looking ahead, gradual normalization of international operations, easing Pratt & Whitney-related groundings, fleet expansion (including A321XLR-led international deployment), and resilient demand trends are expected to support performance recovery over the coming quarters.

* We expect its revenue/EBITDAR to clock a CAGR of 13%/46% over FY26-28. We value the stock at 9x FY28E EBITDAR to arrive at our TP of INR5,600. Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412