Buy Inox Wind Ltd For Target Rs.110 by Motilal Oswal Financial Services Ltd

New order visibility remains strong

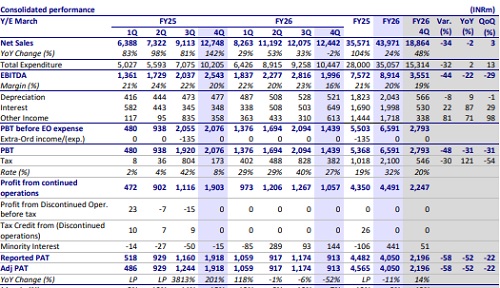

* Weak 4Q: Inox Wind (IWL) missed our revenue est. by 34% at INR12.4b in 4QFY26. EBITDA stood at INR2b as EBITDA margin fell to 16% (vs. 23%/20% in 3QFY26/4QFY25). Adjusted PAT came in at INR0.9b, 58% below estimates. IWL missed its FY26 revenue guidance (incl. other income) of INR50b by 9%. FY26 revenue/ EBITDA/APAT stood at INR43.9b/INR8.9b/INR4.0b (+24%/+18%/-11% YoY).

* Key things we liked about the result:

1) The visibility of recurring captive order inflows from Inox Clean, which plans to add 3GW of renewable capacity annually with 20-30% expected to be wind-based (~1/3rd of IWL’s annual execution target)

2) Management’s strategy to gradually increase pure equipment supply contracts’ share in the order book from ~27% currently to 75% over time, which should improve working capital efficiency and margins

3) Management’s FY27 revenue growth guidance of 75% YoY with EBITDA margins of 20-22%.

* Key monitorables:

1) Relatively weak order inflows, with only 600MW of new orders secured during FY26

2) The company’s inability to meet its FY26 revenue guidance (9% miss).

* Cut FY27/FY28 EBITDA estimates by 7%/6%: We lower our FY27/FY28 EBITDA estimates by 7%/6% as we estimate deliveries to be lower at 1.2GW/1.4GW in FY27/28.

* Valuation : We maintain our BUY rating, given attractive valuations, with a revised TP of INR110 per share (based on 20x FY28E EPS).

Highlights of 4QFY26 performance

* FY26 saw the highest-ever wind capacity additions of 6GW, with management expecting 8-10GW annually going forward, driven by RTC, FDRE, and hybrid capacity additions.

* The 3.1GW order book provides over 24 months of revenue visibility. Additionally, recurring captive order inflows are expected from Inox Clean’s annual capacity addition plan of more than 3GW, with 20-30% of the planned additions likely to be wind-based, supporting a steady order pipeline (equivalent to nearly one-third of IWL’s annual execution).

* FY26 revenue (incl. OI) came in at INR46b vs. guidance of INR50b, with the INR4b shortfall attributed to geopolitical supply chain disruption in a key imported component. Management expects recovery in 1Q and 2Q of FY27.

* FY27 consolidated revenue guidance implies 75% growth over FY26, with EBITDA margin guided at 20-22%.

* Inox Green has set out its FY27 EBITDA guidance of INR6b, underpinned by acquisition consolidation, organic additions, and value-added services.

Valuation and view

* Based on a valuation multiple of 20x FY28E EPS, we arrive at a TP of INR110 per share. Maintain BUY on attractive valuations.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412