Trade Deficit : Export decline leads to higher deficit; FY27E CAD/GDP at 1.7% by Emkay Global Financial Services

Goods trade deficit rose to an eight-month high of ~$30bn in Jun-26 (May-26: ~$28bn), as exports fell 11% mom while imports declined 4% mom. Oil imports and exports fell 15% mom and 42% mom, respectively, as oil prices collapsed following the US-Iran MoU. Gold and silver imports also fell sharply (42% mom and 20% mom, respectively), as global prices dropped. 1QFY27 exports rose 16% yoy, while imports rose 20% yoy. Net services exports fell to $15.1bn in Jun-26, with those for May-26 significantly revised downward; growth has slowed meaningfully over the past few months. We lower FY27E CAD/GDP to 1.7%, assuming average Brent at $90/bbl. While oil prices have fallen following the US-Iran MoU, there is still a possibility of prices spiking again if the ongoing situation escalates. Nevertheless, prices are likely to stay lower for the rest of FY27; at $80/bbl average Brent for FY27, our CAD/GDP forecast falls to 1.4%.

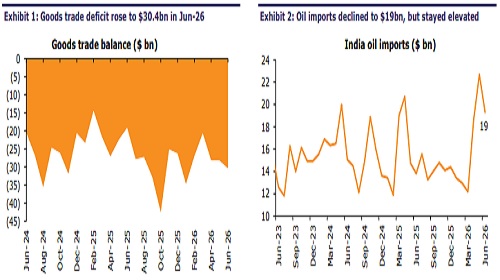

Goods deficit rises to 8-month high as exports fall more than imports

Goods trade deficit rose to an eight-month high of $30.4bn (vs $28.2bn in May-26), with exports falling ~11% mom (+16% yoy) to $40.4bn, while imports fell ~4% mom (+31% yoy) to $70.8bn. Oil imports declined to $19.3bn (-15% mom) as oil prices collapsed after the US-Iran MoU. Similarly, oil exports also fell, by 42% mom to $4.9bn. Gold imports fell 42% mom to $2bn, while silver imports declined 20% mom to $0.1bn. This reflected the import duty hike in May, along with a sharp drop in global gold and silver prices in Jun-26 following the US-Iran peace deal. Thus, for 1QFY27, total goods exports stood at $129bn (16% yoy) with goods imports at $216bn (20% yoy), leading to a goods deficit of $87bn (vs $69bn in 1QFY26). Export diversification efforts continued to bear fruit, with strong yoy growth in exports to Tanzania (146%), Singapore (101%), South Africa (77%), Malaysia (74%), and Vietnam (49%), among others. Exports to China rose 28% yoy during 1Q, while exports to the US were flat yoy.

Core deficit rises with rise in core imports; export trends remain strong

Core (non-oil, non-precious metals) exports dipped 3% mom (+15% yoy) to $33.1bn, while core imports rose 5% mom (30% yoy) to $49.5bn. As a result, core deficit increased to $16.3bn (vs $13bn earlier). Electronic goods exports slowed slightly (-3% mom) to $4.9bn, albeit remaining strong on yoy basis (19%). Electronics goods imports rose on the other hand (9% mom, 59% yoy), to $13.4bn. Other major core export categories (drugs and pharma, chemicals) saw moderate growth momentum, while yoy growth remained healthy. For 1QFY27, core exports have logged at $99bn (13% yoy) with core imports at $144bn (17% yoy), leading to a core deficit of $45bn (vs $35bn in 1QFY26). Despite the healthy growth in engineering and electronic goods exports in 1QFY27, the higher imports of electronic goods and machinery have led to the core deficit widening further.

Services surplus falls in Jun-26; May-26 revised down sharply; growth slowing

Services surplus declined to $15.1bn in Jun-26 (-4% mom, -7% yoy), with the May-26 surplus being significantly revised down to $15.7bn from $17.7bn. As a result, provisional net services exports for 1QFY27 came in at $49bn, up only 3% yoy, with gross services exports ($54bn) rising 9% yoy. For Jun-26, exports ($33bn) rose 3% yoy, while imports ($17.9bn) were up 13% yoy. Net services exports growth has slowed sharply in recent months, in the face of AI headwinds, and further growth moderation would create upside risks for CAD/GDP

FY27E CAD/GDP at 1.7%/1.4% at average Brent of $90/$80/bbl, respectively

We expect CAD/GDP to worsen to 1.6% in 1QFY27 (4QFY27: 0.7% surplus), due to a higher goods trade deficit (led by higher oil imports) and a moderation in remittances and net services exports. We lower FY27E CAD/GDP to 1.7% at $90/bbl average Brent prices, assuming lower oil imports vs earlier. While oil prices fell sharply to ~$70/bbl following the US-Iran peace deal in June, they have ticked up to ~$79/bbl after hostilities resumed this week, with the return of a full-fledged conflict likely to see prices cross $90/bbl once again. Nevertheless, there is still a likelihood of prices staying lower for the rest of FY27; FY27E CAD/GDP is expected to be 1.4% at $80/bbl average Brent price for the year.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354

More News

Market is expected to open on a gap down note and likely to witness range bound move during ...