The Economy Observer : A big bang policy! by Motilal Oswal Financial Services Ltd

* The RBI and the government have executed a well-choreographed move to attract foreign capital. The measures include the addition of new long-term G-sec securities under the fully accessible route, incentivizing of ECB borrowing for PSUs, allowing for fresh FCNR (B) deposits, and reducing the withholding tax rates to 0% from the current 20% on capital gains in the debt market. Together, these measures are likely to boost fresh inflows by USD30-50b in FY27, supporting the rupee, which trades with an appreciation bias, as well as bonds, which are expected to remain sub-7% post-policy.

* The initiative also paves the way for India to negotiate inclusion in global bond indexes, which could serve as another near-term positive trigger if finalized.

* We continue to expect a cumulative 50bp rate hike in FY27. However, if elevated oil prices, currency pressures, and inflation risks persist, the probability of policy tightening is likely to increase from 3QFY27 onwards. Until then, the RBI is expected to remain data-dependent and utilize non-rate measures to manage external-sector risks.

Key highlights from RBI Jun’26 policy:

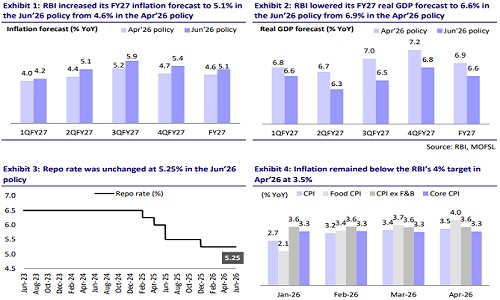

* The Reserve Bank of India’s Monetary Policy Committee (MPC) unanimously kept the repo rate unchanged at 5.25% and reiterated its Neutral stance. The decision reflects a cautious approach amid heightened global uncertainty, providing the RBI with flexibility to respond to evolving growth and inflation dynamics while assessing the impact of recent external shocks.

* The MPC noted that India’s macroeconomic fundamentals remain resilient, supported by robust private consumption, government capex, healthy credit growth, and continued strength in manufacturing and services activity. However, the escalation of the West Asia conflict, elevated energy prices, and supply-chain disruptions have worsened the external environment. Consequently, the RBI revised its FY27 GDP growth forecast down to 6.6% from 6.9% projected in April, with growth projected at 6.6%/6.3%/6.5%/6.8% in 1Q/2Q/3Q/4QFY27, respectively. Risks remain tilted to the downside due to prolonged geopolitical tensions, weaker global demand, higher energy costs, and weather-related uncertainties.

* While headline inflation remained below the RBI’s target during March-April 2026, the inflation outlook has deteriorated materially. The RBI raised its FY27 CPI inflation forecast to 5.1% from 4.6% in the April policy, with quarterly projections at 4.2%/5.1%/5.9%/5.4% in 1Q/2Q/3Q/4QFY27. The upward revision primarily reflects higher crude oil prices (USD95/bbl vs. USD85/bbl in Apr’26 policy), rising input costs, supply chain disruptions. and weather-related risks associated with a below-normal monsoon and potential El Niño conditions.

* The RBI flagged rising weather-related inflation risks, with the Southwest monsoon forecast at 90% of LPA and El Niño conditions likely to emerge. The Central Bank noted that recent fuel price increases could add around 36bp to headline CPI inflation, while a weaker monsoon could create additional upside risks to food inflation despite comfortable foodgrain stocks.

* The RBI highlighted that although underlying inflation pressures remain relatively benign, second-round effects through wages, inflation expectations, and broader price-setting behavior remain the key concerns. Core inflation is projected at 4.7% in FY27 (4.4% in Apr’26 policy), although core inflation excluding precious metals remains considerably lower, suggesting that demand-side inflation pressures remain contained at present. This assessment is consistent with the risks highlighted in our report, ‘Consumption Risks and Opportunities’, where we argued that the primary macroeconomic impact of a weak monsoon is likely to be transmitted through higher food inflation and weaker rural purchasing power rather than a sharp decline in agricultural output/real GDP growth. Higher food inflation disproportionately affects rural households, compressing real incomes and posing downside risks to rural consumption, particularly for FMCG, entry-level automobiles, consumer durables, and other rural-facing sectors.

* Liquidity conditions remain in surplus, with the average daily system liquidity surplus standing at INR2.6t since the April policy. However, surplus liquidity has moderated significantly over recent months, declining from INR3.7t in April to INR1.7t in May and INR1.4t in early June, indicating a gradual normalization of banking system liquidity. Despite this moderation, liquidity remains adequate to support credit growth, which continues to be robust at 16.2% YoY (as of 15th May’26). RBI expects a drawdown of government cash balances post-surplus transfer and currency return during the monsoon to aid banking system liquidity in the near term. RBI will continue to ensure appropriate liquidity for productive requirements and further monetary policy transmission.

* Our view: The RBI has adopted a cautious approach, balancing rising inflation risks against a weakening growth outlook. While the policy tone has become more hawkish, the RBI is currently relying on capital-flow measures, FX intervention, and liquidity management to support the rupee and maintain macroeconomic stability rather than immediately raising rates. We continue to expect a cumulative 50bp rate hike in FY27. If elevated oil prices, currency pressures, and inflation risks persist, the probability of policy tightening is likely to increase from 3QFY27 onwards. Until then, the RBI is likely to remain data-dependent and utilize non-rate measures to manage external-sector risks.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412