Sell Tata Elxsi Ltd for the Target Rs. 3,350 by Motilal Oswal Financial Services Ltd

Guidance resets as vertical recovery uneven

Deal ramp-up delays weigh on the growth

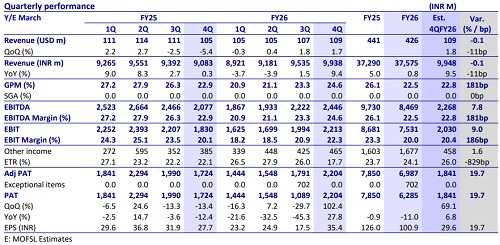

* Tata Elxsi (TELX) reported revenue of USD109m in 4QFY26, up 0.9% QoQ in CC terms, below our estimate of 2.0% CC. Growth was led by media and communication business (up 5.6% QoQ CC), whereas HLS declined 13.1% QoQ CC. EBIT margin was 22.3% (up 140bp QoQ), above our estimate of 20.4%. Adj. PAT was up 23.1%/27.8% QoQ/YoY to INR2,204m (above our est. of INR1,841m).

* For FY26, revenue grew 0.8% YoY, while EBIT/adj. PAT declined 13.2%/11% YoY in INR terms compared to FY25. We expect revenue/EBIT/adj. PAT to grow by 15%/32.6%/36.8% YoY in 1QFY27. FY26 RoE came in at 21.3% (vs. 29.3%/34.5%/41.0% in FY25/FY24/FY23).

* TELX’s outlook has turned more conservative, with FY27 growth guided to be in high-single digits amid delayed deal closures and elongated decision cycles. We value the stock at 22x FY28E EPS, with a TP of INR3,350. We reiterate our Sell rating.

Our view: Transportation strength helps; HLS is likely to be bottomed out

* Near-term growth moderated; demand remains mixed: 4QFY26 revenue growth of ~0.9% QoQ CC reflects a subdued exit, with delays in deal closures and elongated decision cycles weighing on momentum. Management has lowered FY27 outlook to high-single-digit growth, suggesting limited near-term visibility (we build in 7.3% YoY cc growth for FY27). While deal wins continue, conversion into revenue remains uneven, indicating a mixed demand environment.

* Deal wins intact, but ramp-up timing is key: The company continues to win across verticals, including new logos in Transportation and a large consolidation deal in Media & Communication. However, new deals typically take 9–12 months to scale, and some Healthcare deals slipped into 1Q. We believe growth in FY27 will be driven by the ramp-up of existing wins and wallet share expansion.

* Transportation steady; HLS likely bottoming out: Transportation remains the key driver, supported by OEM-led engagements and rising offshoring. Media & Communication continues to witness cost-takeout-driven spends amid industry consolidation. Healthcare & Life Sciences growth was impacted by timing delays, but management indicated 4Q as the trough, with a recovery expected from 1Q. We see early signs of stabilization, though growth is likely to remain uneven across verticals.

* Margins supported by utilization; gradual improvement ahead: EBITDA margin expanded to 24.6%, aided by currency tailwinds and operating leverage, particularly utilization gains. While fixed-price contracts and pyramid optimization are supporting margins, wage hikes, and deal rampup costs could limit sharp upside. Management targets ~27% exit margin in FY27, we expect margin normalization to be gradual as deal ramp-ups, hiring, and continued investments in GenAI and domain capabilities resume. We expect 25.0% margin for FY27.

Valuations and changes to our estimates

* While 4QFY26 saw modest growth, TELX’s outlook has turned more conservative, with FY27 growth guided to be in high-single digits amid delayed deal closures and elongated decision cycles. Growth remains dependent on ramp-up of existing deals and Transportation-led momentum, while Media and Healthcare recovery is gradual. We expect USD revenue growth to remain moderate at ~7% CAGR over FY26–28.

* We have modestly revised our estimates for FY27/FY28 by 1%. Margin expansion is expected to be gradual and back-ended, with EBIT margins expanding to 23.7%. We value the stock at 22x FY28E EPS, with a TP of INR3,350. We reiterate our Sell rating.

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

600-400.jpg)