Sell Fine Organic Industries Ltd for the Target Rs 3,980 by Motilal Oswal Financial Services Ltd

Healthy performance amid persistent macro headwinds Earnings above our estimate

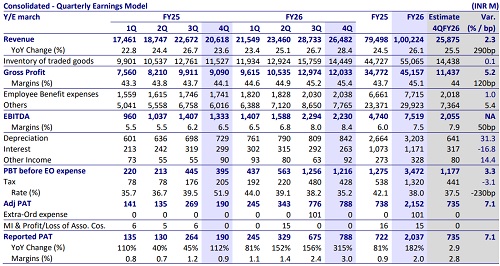

* Fine Organic Industries (FINEORG) reported healthy operating performance, with an EBITDA growth of 9% YoY, primarily due to gross margin expansion of 70bp YoY to 40.3%.

* Fine Organic Industries continues to strengthen its global footprint through expansion into new geographies and strategic partnerships. In line with this strategy, the Board has approved the acquisition of Oleofine Organics, Malaysia (engaged in the manufacturing and sale of specialty chemical products), further reinforcing the company’s international expansion plans.

* However, we expect FINEORG’s operating performance to remain affected by macroeconomic uncertainties, supply chain disruptions, rising raw material costs, and capacity constraints across facilities.

* We broadly retain our earnings estimates for FY27/FY28 and estimate a revenue/EBITDA/Adj. PAT CAGR of 9%/7%/4% for FY26-FY28. FINEORG currently trades at ~31x FY28E EPS and ~23x FY28E EV/EBITDA. We value the stock at 27x FY28E EPS (~20% discount to the five-year avg. P/E of 33.6), to arrive at our TP of INR3,980. Reiterate Sell.

Margin expansion led by stable demand

* FINEORG reported revenue of INR6.2b in 4QFY26, rising 3% YoY. Overall demand remained stable during the quarter, with export markets showing steady performance.

* Export revenue grew 1% YoY to INR3.4b, while domestic revenue grew 5% YoY to INR2.8b, driven by improved domestic demand.

* Gross margin stood at 40.3% (up 70p YoY), while EBITDA margin expanded 110bp YoY to 20.8% in 4QFY26.

* EBITDA stood at INR1.3b, up 9% YoY, and Adj. PAT grew 21% YoY to INR1.2b in 4QFY26 (est. of INR919m).

* In FY26, its revenue/adj. PAT grew 4%/2% YoY to INR23.7b/INR4.2b, while EBITDA declined 4% to INR4.9b.

* CFO stood at INR4.3b as of Mar’26, compared to INR2b in Mar’25.

Valuation and view

* The company remains focused on strengthening its global presence through investments in overseas subsidiaries, expanding US capacity for future growth, enhancing manufacturing capabilities, incorporating a wholly-owned subsidiary in Dubai to establish a local presence in GCC countries, and expanding its presence in Malaysia with the acquisition of Oleofine Organics.

* We anticipate FINEORG performance to be adversely affected by the following factors:

1) longer-than-expected delays in the commissioning of new capacities for expansion

2) existing plants operating at close to optimum utilization, with no potential for debottlenecking

3) the macroeconomic environment.

* We broadly retain our earnings estimates for FY27/FY28 and estimate a revenue/EBITDA/Adj. PAT CAGR of 9%/7%/4% for FY26-FY28. FINEORG currently trades at ~31x FY28E EPS and ~23x FY28E EV/EBITDA. We value the stock at 27x FY28E EPS (~20% discount to the five-year avg. P/E of 33.6) to arrive at our TP of INR3,980. Reiterate Sell.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412