Rollover Analysis – February 2026 by Systematix

Index Weakness with Stock-Level De-risking

February expiry marked a stabilisation phase with Nifty gaining nearly 1% and breadth improving materially, while rollover moderation and softer index carry signalled easing of earlier bearish conviction. Nifty futures recorded the lowest rollover in a year, indicating long unwinding at the index level, whereas Bank Nifty showed fresh long buildup with higher rollover and expanding open interest, reinforcing its leadership. Sectorally, positioning rotated toward Power, Oil Gas, Construction and Capital Goods with clear long buildup, while Information Technology and Consumer Services continued to reflect short buildup and long unwinding. FIIs reduced index shorts but increased stock-level exposure, highlighting a shift toward selective positioning in a higher-volatility environment. For the current series, the focus remains on stock-specific opportunities, with BEL, OIL, NMDC and ICICIPRULI emerging as key stocks to watch based on rollover strength, open interest expansion and supportive sector alignment.

Index Performance & Market Breadth

February expiry turned positive for the first time in the last six expiries, with Nifty gaining nearly 1% and marking a fresh lifetime high following the trade deal announcement on 3 February. Market breadth improved materially, with 145 advances against 61 declines, indicating broader participation compared to previous months. BankNifty maintained its relative strength, closing higher for the sixth consecutive expiry with a gain of 2.93% and registering a new all-time high during the month, reinforcing continued leadership.

Sectoral Dispersion During the Expiry

Fourteen out of eighteen sectors closed positive by market capitalisation during the February expiry, reflecting broad-based strength. Power (up 14.8%), Services (up 12.6%), Construction (up 10.4%) and Capital Goods (up 10%) emerged as the top performers by market cap. In contrast, Information Technology was the standout laggard, declining sharply by 21%, marking the most significant sectoral correction of the expiry. From a positioning standpoint, the highest open interest expansion by value was observed in Power (up 17%), Oil, Gas & Consumable Fuels (up 10.4%) and Construction (up 10%), indicating fresh participation and carry-forward interest in these segments. On the other hand, meaningful unwinding was visible in Consumer Services (down 12%), Textiles (down 11%) and Realty (down 10%), suggesting profit booking and position reduction in previously active pockets.

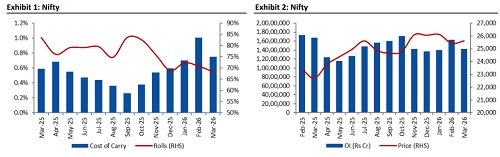

Nifty Futures Rollover Diagnosis

February expiry recorded the lowest rollover of the past one year at 68%, compared with 71% in January and the three-month average of 71%. The new series opened with an open interest base of 1.42 crore shares, approximately 20 lakh shares lower than January, indicating a meaningful reduction in carried-forward positions. Expiry-day rollover cost declined to 75 basis points from 101 basis points in the previous series. The combination of lower rollover, reduced open interest and softer cost of carry points toward long unwinding rather than fresh short buildup, suggesting that the earlier bearish conviction has moderated and leveraged positions have been trimmed at the index level.

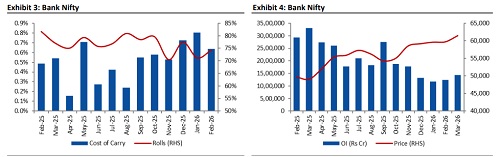

Bank Nifty Futures Rollover Diagnosis

Bank Nifty rollover improved to 74%, compared with 71% in the previous expiry and above the three-month average of 73%. The new series began with open interest at 14.28 lakh shares, the highest level observed in the last three months and approximately 1.88 lakh shares higher than January, signalling strong carry-forward interest. With the index closing in positive territory alongside expanding open interest, the data indicates fresh long buildup in Bank Nifty futures. In contrast to the moderation seen in Nifty futures rollover, Bank Nifty continues to attract positional participation, reinforcing its relative strength and sustained leadership within the broader market structure

Above views are of the author and not of the website kindly read disclaimer