Reduce Gabriel India for the Target Rs. 1,050 by Choice Institutional Equities

Strong execution across core businesses supports growth momentum:

GABR delivered a healthy topline performance in Q4FY26, driven by a strong traction across 2W, PV, CV and sunroof businesses. Consolidated revenue grew by 12.7%, supported by healthy OEM demand, aftermarket growth and improving contribution from the sunroof business. However, margin and profitability remained affected due to elevated commodity costs, volatile aluminium prices, gas shortages and supply chain disruptions in this quarter. The recently approved restructuring scheme marks a strategic transition for GABR from a suspensionfocussed manufacturer to a diversified mobility solutions provider through the consolidation of Dana Anand, Henkel Anand, ACYM and Anchemco. We believe the addition of driveline products, NVH solutions, aluminium forgings, synchronizer rings, coolants and brake fluids significantly strengthens GABR’s long-term growth visibility and reduces dependence on a single product category.

Sunroof and new mobility businesses to drive growth: Sunroof business remained a key growth driver with FY26 revenue at ~INR 4.34 Bn and EBITDA margin at ~15.1%, while capacity doubled to ~400k units annually. GABR is also expanding into solar dampers, EV fluids and automotive fasteners through strategic JVs. However, commodity inflation, slower PV ramp-up and execution risks in scaling up new businesses could continue pressuring near-term margin and earning visibility.

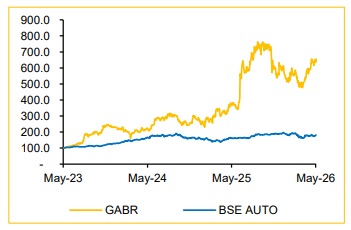

View and Valuation: We largely maintain our FY27/28E EPS estimate. We value the company at 28x (maintained) P/E multiple on FY28E EPS and maintain our target price of INR 1,050. We downgrade the stock from ‘BUY’ to ‘REDUCE’, given the sharp rally in the stock price, which has left limited room for an upside. While the ongoing restructuring is a catalyst for FY27E growth, we believe this is fully priced in at the current level.

Q4FY26: Result is in line with our estimate

* Revenue was up 12.7% YoY and up 2.6% QoQ to INR 12,096 Mn (vs CIE estimate of INR 12,041 Mn)

* EBITDA was up 3.9% YoY and up 5.7% QoQ to INR 1,130 Mn (vs CIE estimate of INR 1,096 Mn). EBITDA margin was down 80 bps YoY and up 27 bps QoQ to 9.3% (vs CIE estimate of 9.1%)

* APAT was up 4.0% YoY and down 1.5% QoQ to INR 669 Mn (vs CIE estimate of INR 678 Mn)

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131