Paints Sector Update : Pricing action underway ; demand recovery outlook appears bleak by Motilal Oswal Financial Services Ltd

Geopolitical tensions leading high pricing in slow demand trend

* Paint companies have initiated price hikes to negate cost inflation arising from ongoing geopolitical challenges. The paint sector is relatively high sensitive to crude price movements, as crude - linked derivatives (solvents, resins, binders, and phthalic anhydride, etc) constitute ~40% of the raw material basket. This high dependence directly exposes gross margins to oil price volatility. Berger Paints, Indigo Paints, and Kansai Nerolac have initiated price hikes of ~3%. Asian Paints has announced a 6 - 8% price hike from 10th April onward. Berger Paints has also announced a second phase of price hike of 5-10% from 9th April. Our checks suggest that most other paint companies are also planning a second round of price hikes in early April.

* The geopolitical situation remains uncertain, and supply normalization is likely to take time even after war-related conditions ease. Therefore, cost inflation is expected to persist in the near term, and paint companies are unlikely to roll back prices quickly (particularly amid seasonal demand). Trade discounts/schemes have increased significantly to 20 - 22% from historical levels of 12-13% (three years back). Companies may opt to reduce trade schemes if cost inflation sustains.

* Demand has steadily improved over the last five months post weak demand last October. This trend has sustained over the last three weeks (post geopolitical tensions), with the possibility of partial trade pre - buying in March. Given existing RM and FG inventory, recent cost inflation is unlikely to affect 4QFY26 performance. The impact will be more visible in 1QFY27, post price hike-led demand impact.

* Overall, consumption trends have remained muted over the last 2 - 3 years, we were expecting recovery in FY27 supported by multiple macro initiatives. However, if inflation rises further, the consumption cycle could see a delayed recovery. As festivals in FY27 fall in mid-November, the paint industry may benefit from an extended period of post - monsoon demand, unlike last year when demand was impacted by early festivities (mid-October) and extended monsoon. Accordingly, while the possibility of paint demand recovery remains intact, ongoing macro uncertainties and 8–10% price hikes have led us to moderate our volume growth assumptions for Asian Paints and Indigo Paints. Additionally, margin pressures are expected to weigh on profitability, resulting in EPS cut of 4 - 6% for Asian Paints and 3 - 7% for Indigo Paints for FY27 and FY28. We maintain our Neutral rating on Asian Paints with TP of INR2,450 and BUY on Indigo Paints with TP of INR1,100.

Paint players implementing calibrated price increases to offset RM pressure

The industry has entered a broad-based and calibrated price hike cycle to mitigate input cost pressures.

* Asian Paints, the market leader, has announced a 6 - 8% price increase in two phases. In the first phase, the company will increase price in key decorative categories, such as emulsions, enamels, primers, and distempers, w.e.f. 10th Apr’26. The second phase will begin from 21st Apr’26, covering waterproofing, adhesives, and wood finishes.

* Berger Paints has implemented the first phase of a ~3% price hike, effective from 25th March, with an announcement made to implement the second phase of 5–10% from 9th April.

* Other players, such as Indigo Paints and Kansai Nerolac, have also implemented ~2–3% price hikes and are planning additional increases in April.

Promotions and trade schemes to play a role in indirect pricing

In addition to direct price hikes, companies are increasingly leveraging trade discount rationalization to support realizations. Over the past 2 - 3 years of benign crude prices, competitive intensity has led to a significant expansion in trade schemes, which increased to 20-22% from historical levels of 12 - 13%. As input costs rise, companies are reducing promotional schemes and using them as an indirect pricing lever. This strategy supports margin while minimizing the immediate impact of headline price hikes on end-consumer demand.

Checks suggest a sequential improvement in demand in 4Q

Demand has steadily improved over the last five months following weak demand last October. The same has sustained over the last three weeks (post the geopolitical tension), with the possibility of partial trade pre-buying in March. Given the RM and FG inventory, recent cost inflation is unlikely to impact 4QFY26 performance. The impact will be more visible in 1QFY27, post price hike-led demand impact. Overall, consumption trends have remained muted during the last 2 - 3 years, though we expect consumption recovery in FY27, supported by multiple macro initiatives. However, if inflation rises further, the consumption cycle may experience delayed recovery. We model consolidated revenue/volume growth of 5%/9% for Asian Paints and revenue growth of 10% for Indigo Paints in 4QFY26.

Learnings from the Russia - Ukraine conflict

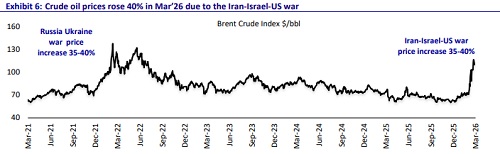

* A similar cost inflation cycle was observed during the Russia - Ukraine war, when crude prices surged sharply by 35 - 40% to ~USD 140/bbl (2021 -2022), significantly increasing input costs for paint companies. During this period, most players implemented calibrated price hikes.

* Leading players such as Asian Paints implemented cumulative price increases of 20 - 25%, with peers such as Berger Paints, Indigo Paints, Kansai Nerolac, and Akzo Nobel also raising prices by ~20%. Despite these measures, gross margins contracted 450 - 500bp (adjusted for the elevated COVID base driven by sharp RM deflation), primarily due to a lag in pass-through. Margins, however, recovered over the subsequent 3 - 4 quarters, supported by easing raw material prices and pricing actions.

RM sensitivity to crude; assessing price hike requirement

* Paint companies are sensitive to crude movements, as crude - linked derivatives (solvents, resins, binders, and phthalic anhydride) account for ~40% of their raw material basket. This high dependence directly exposes gross margins to oil price volatility.

* Using a base crude assumption of USD68.5/bbl (1HFY25 average), we model scenarios in which crude rises to USD85 - 110/bbl, potentially resulting in sharp RM inflation of 25 - 60% YoY, while general (non - crude) inflation remains relatively moderated at 5 - 8%. To offset this cost pressure, companies are implementing price hikes. However, given the lag in passing on higher costs, gross margins may experience near-term pressure.

Our view: High RM sensitive, earnings pressure likely

* Paint consumption trends have remained muted over the last 2 - 3 years, we were expecting recovery in FY27 supported by multiple macro initiatives. However, if inflation rises further, the consumption cycle could see a delayed recovery. As festivals in FY27 fall in mid - November, the paint industry may benefit from an extended period of post-monsoon demand, unlike last year when demand was impacted by early festivities (mid - October) and extended monsoon.

* Accordingly, while the possibility of paint demand recovery remains intact, ongoing macro uncertainties and 8 - 10% price hikes have led us to moderate our volume growth assumptions for Asian Paints and Indigo Paints. Additionally, margin pressures are expected to weigh on profitability, resulting in EPS cut of 4 - 6% for Asian Paints and 3 - 7% for Indigo Paints for FY27 and FY28. We maintain our Neutral rating on Asian Paints with TP of INR2,450 and BUY on Indigo Paints with TP of INR1,100.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

.jpg)