Oil & Gas Sector Update : Strait of Hormuz disruption: Upstream positive; OMCs/CGDs at risk Motilal Oswal Financial Services Ltd

Heightened geopolitical tensions in the Middle East and reports of potential disruption at the Strait of Hormuz (SoH) have materially increased uncertainty around global energy flows. Given the strategic importance of the SoH to crude, product, and LNG trade, we outline the key developments and assess the potential implications for commodity prices and sectoral earnings

SoH - what we know so far and the potential impact:

* Iranian media has reported that the SoH has been closed (media article). If confirmed, this would be an unprecedented event, marking the first such instance in the past 54 years. In addition, there appears to be a broader media consensus that vessels are actively avoiding transit through the SoH amid rising tensions.

* 15%/8%/20% of global crude/refined product/LNG flows through SoH: The SoH is one of the most critical energy chokepoints globally. ~15/6 mbpd of crude oil and refined products transit through the SoH, accounting for nearly 15% of global crude consumption and around 8% of global refined product consumption. Further, nearly 20% of global LNG trade moves through the SoH, including almost all LNG exports from Qatar and the UAE.

* Alternative routes provide limited buffer: While alternatives exist, they can likely handle only ~7-8 mbpd of crude/refined products vs ~21 mbpd currently transiting the SoH. Diversions would also entail meaningfully higher freight costs.

* Potential impact of closure: A full or partial Iranian blockade could lead to a sharp increase in crude prices, refining GRMs, and spot LNG prices.

Upstream and shipping sectors likely beneficiaries:

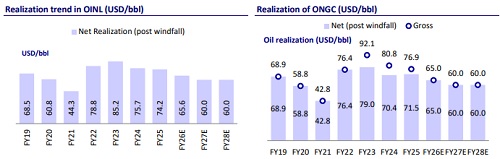

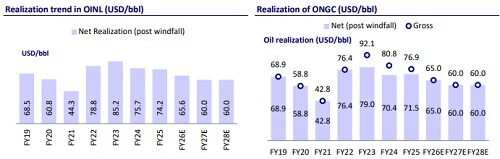

? Upstream players - earnings leveraged to crude upside: Upstream companies could benefit from higher crude prices. There is currently no windfall tax in place, and Brent is already trading close to USD75/bbl. While we have a Neutral rating on both ONGC and Oil India, note that a USD5/bbl change in oil prices impacts FY27 standalone EBITDA by ~8% for ONGC and ~11% for Oil India.

? Shipping companies - geopolitical disruption supportive for charter rates: Shipping companies are also likely to benefit, as geopolitical disruptions typically tighten vessel availability and support charter rates. The sector has already witnessed strong performance over the past five years amid elevated freight rates. ~40–45% of GE Shipping Company’s shipping fleet comprises oil and product tankers.

? Standalone refiners to benefit from potentially higher refining cracks: MRPL and MRL (Chennai Petroleum) (not rated) could also benefit amid high refining cracks and possible inventory gains.

OMCs, CGDs, and gas utilities likely negatively impacted:

* OMCs are likely to face headwinds: A potential USD10/bbl spike in crude prices could erode marketing margins by ~INR4.5/lit, with only partial offset from improved refining margins and possible inventory gains. In addition, propane prices have already risen by ~USD75/ton MoM to USD600/ton amid ongoing supply disruptions from Saudi Arabia.

* Pressure on CGD margins: Higher Brent and spot gas prices imply elevated gas sourcing costs, pressuring margins.

* Gas utilities - limited near-term impact; risk if spot LNG remains elevated: For gas utilities such as GAIL and PLNG, we see limited immediate impact at this stage. However, if the situation persists for a prolonged period and leads to sustained elevation in spot LNG prices, earnings could be negatively impacted due to higher sourcing costs and potential demand-side pressure.

* Neutral to marginally positive for Reliance Industries: We could see a minor positive impact for Reliance Industries, should refining margins strengthen. Additionally, the company’s ability to source multiple feedstocks for its petrochemical operations provides operational flexibility amid commodity price volatility.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412