Oil and Gas Sector Update : Crude Compass: IEA Response to Supply Fears by Choice Institutional Equities

What has happened:

* Brent prices are trading around USD97/b (up 5% from March 11, 2026) at the time of writing of this report.

* IEA has released 400 million barrels of crude oil into the market. However, the discharge rate remains capped at 2 million barrels per day (mbd). During the Russian – Ukraine war, the rate of discharge was approximately 1.1mbd.

* Three vessels in the Strait of Hormuz have been attacked on 11th March 2026. The shipments through the Strait of Hormuz remains close to zero.

In our opinion:

* In the current market conditions, as Strait of Hormuz remains closed, for the market to rebalance, roughly 20 million barrels of demand destruction may be required – a level we believe could occur if Brent reaches above USD130/b. The balancing threshold is elevated because the supply deficit is likely to widen in the near term as: (a) floating inventories (oil on water) decline over the coming weeks, (b) flows through the Strait of Hormuz remain disrupted, and (c) curtailed production will require ~15–20 days to ramp up even after maritime transit resumes.

* To explain the current oil price environment, we split the trajectory of rise in oil prices into three parts: (i) the initial supply shock (below USD 90/b), (ii) precautionary demand necessitated by hoarding and inventory builds (USD 90 to 130/b), and (iii) a scarcity premium that ultimately forces demand destruction (beyond USD 130/b).

* Despite a physical disruption of 7–11 mb/d, the surge in Brent suggests the market is pricing a much larger effective deficit of ~20 mb/d, reflecting precautionary demand and panic-driven hoarding to gather pace over the coming days

* Provided Hormuz maintains status-quo into 4 th week without negotiations between US-Israel and Iran in place, the market may enter the scarcity-premium phase as floating inventories diminish and marginal storage tightens. In such a scenario, price moves tend to accelerate sharply, which could push Brent towards ~USD 130/b by end of next week.

Bear case scenario:

* If US-Israel intervention leads to renewed negotiations and the reopening of the Strait of Hormuz, Brent prices could retreat towards ~USD 80/b over the coming weeks. This would largely reflect the unwinding of the precautionary demand premium, although a residual geopolitical risk premium may persist. Implication on Indian Refineries and OMCs

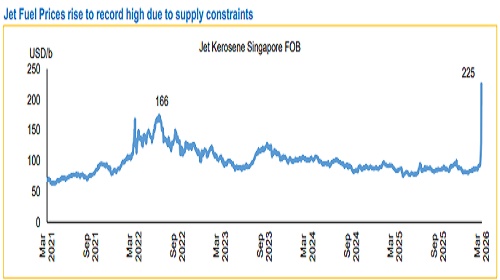

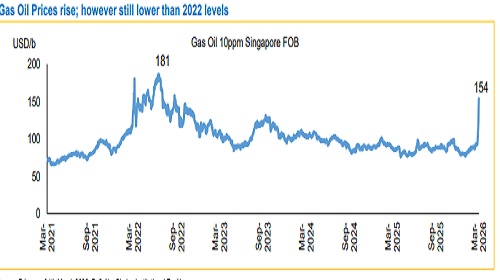

* For Indian equities, the surge in diesel cracks is supportive for pure-play refiners. Data from the Petroleum Planning and Analysis Cell shows international Diesel (FOB) prices rising 65% MTD in March to USD 142.34/b, versus USD 86.03/b in February. As opposed to this, Brent has increased ~25%. This divergence implies stronger refining margin for pure-play refiners relative to integrated OMCs. Meanwhile, at the current price level, the marketing margin turns negative for OMCs. We raise our Brent estimate for Calendar Year 2026 from USD61.5/b to USD66/b, as previous estimate was based on catalyst that Russia – Ukraine war to end and possible lifting of sanctions on Rosneft and Lukoil. However, it is significantly delayed. Moreover, based on geopolitical developments, we have raised our estimate.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131