Neutral Torrent Pharma Ltd for the Target Rs 4,400 by Motilal Oswal Financial Services Ltd

In-line debut with JBCP; highest IPM growth among top 10 Multiple levers intact – JBCP synergies, Semaglutide scale, Brazil pipeline

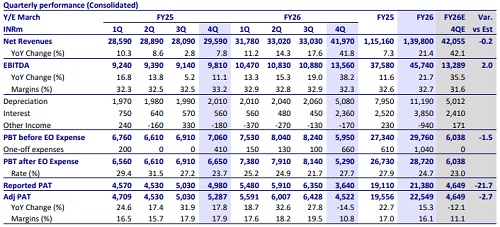

* Torrent Pharma (TRP) delivered in-line financial performance in 4QFY26. It was the first quarter with consolidated financials after the acquisition of JB Chemicals and Pharma (JBCP). Excluding JBCP, TRP delivered 16% YoY growth in revenue and EBITDA.

* TRP’s base domestic formulation (DF) business grew at the highest rate among the top 10 companies in 4Q. Interestingly, YoY growth was diversified across volume, price hike and new launches.

* Notably, TRP has garnered 38% market share in semaglutide market. TRP has launched oral and injectable versions of the product. Market share gain implies strong prescriptions from healthcare professionals.

* Brazil remained another growth market for TRP, driven largely by new launches. It has a healthy product pipeline to sustain the growth momentum in this segment.

* The favorable regulatory guidelines for introducing biosimilars in Germany market is expected to improve growth prospects for TRP going forward.

* We have factored in the addition of JBCP financials under TRP management and improved growth prospects in branded generics markets of DF and Brazil. We have also considered the addition of TRP equity shares, considering the share swap to non-promoter shareholders of JBCP. As a result, we have revised our EPS estimates to INR66/INR92 for FY27/FY28.

* We value TRP at 45x 12-month forward earnings to arrive at a TP of INR4,400. Considering the current valuation largely factors in the earnings upside, we maintain Neutral rating on the stock.

Strong revenue growth offsets margin pressure

* Sales grew 41.8% YoY to INR42b (our est: INR42b).

* Gross margin contracted 10bp to 75.8%. EBITDA margin contract 90bp YoY to 32.3%, driven by rise in other expenses (up 90bp YoY as % of revenue).

* Accordingly, EBITDA grew 38.2% YoY to INR13.6b (our est: INR13.3b).

* Adj. PAT declined 14.5% YoY to INR4.5b.

* TRP’s base business (excl. JBCP) witnessed 16% YoY growth in revenue and EBITDA. EBITDA margin came in at 32.7%.

* JBCP’s 4Q revenue/EBITDA came in at INRINR7.7b/INR2.4b, with margin at 30.5%.

* For FY26, revenue/EBITDA/PAT grew 21%/22%/15% YoY

Broad-based growth across geographies

* India formulations revenue grew 43% YoY to INR22.2b (53% of sales). Excl. JBCP, TRP’s DF business rose 15% YoY in 4QFY26.

* US generics grew 31% YoY to INR4b (+9% YoY in cc terms; 9% of sales).

* Germany sales grew by 16% YoY to INR3.3b (8% of sales).

* LATAM business grew 30% YoY to INR4.6b (+11% in cc terms; 11% of sales).

* ROW+CDMO sales grew 68% YoY to INR8b (19% of sales)

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412