Neutral SONA BLW Precision Forging Ltd for the Target Rs. 546 by Motilal Oswal Financial Services Ltd

Input cost pressure to hurt margins in the near term

* SONA BLW Precision Forging’s (SONACOMS) 4QFY26 consol. PAT at INR1.9b came in above our est. of INR1.8b, led by better-than-expected revenue growth. Revenue beat was led by a better-than-expected pick-up in BEV revenue in 4Q.

* Considering better-than-expected revenue growth in 4Q, we raise our earnings by 1%/6% for FY27E/FY28E. The global auto demand slowdown and a slower-than-expected EV transition in key markets remain the key concerns for SONACOMS. Thus, while SONACOMS enjoys a healthy order backlog, it may see execution challenges given the expected slower EV transition. The stock at 49x/42x FY27E/FY28E factors in most positives. We reiterate our Neutral rating with a TP of INR546, valued at 38x FY28E EPS.

Healthy sequential pick-up in BEV drives earnings beat

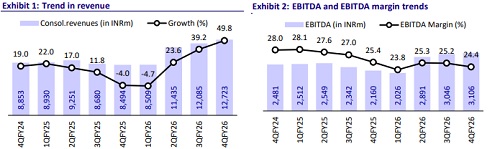

* 4Q revenue grew 50% YoY to INR12.7b (above our estimate of INR12b). While YoY growth was driven by the integration of the Railways business and strong growth in traction and suspension motors, the 5.3% QoQ growth was driven by a strong pick-up in BEV revenue.

* BEV revenue picked up QoQ with the BEV market in North America posting its best-ever monthly run rate in March, ever since the subsidy cuts. BEV contribution improved to 39% in 4Q from 38% in 3Q.

* Margins, however, contracted by 100bp YoY to 24.4%, slightly below our estimates. EBITDA grew ~44% YoY to INR3.1b and was broadly in line with our estimates.

* Adverse product mix and input cost inflation led to a decline in margins YoY. Additionally, 4QFY25 EBITDA had full-year PLI benefit, resulting in a 1.9% positive impact compared to current quarter.

* PAT was up 23.6% YoY at INR1.9b, beating our estimate of ~INR1.8b.

* For FY26, revenue/EBITDA/PAT were up 23.2%/13.5%/9.5% YoY at ~INR44b/INR11b/INR6.8b. Full-year margins, however, were down 170bp YoY at 24.7% due to the integration of the railway business, an adverse product mix and higher input cost pressure in 2H.

* CFO for the year stood at ~INR6.6b, with FCF of INR1.8b. As of FY26 end, the company had a net cash position of INR1.5b.

Highlights from the management commentary

* Geographic diversification continued to strengthen, with eastern markets contributing 60% of 4Q revenue vs. 40% a year ago. India’s contribution crossed 50% of full-year revenue, helping offset weakness in North American passenger vehicle demand.

* Net order book remains healthy at ~INR237b, with EVs constituting nearly 70% of the total. Non-EV wins also remained robust, including seven new differential gear programs from existing customers, reflecting broad-based traction across products, geographies and propulsion technologies.

* The company added three new EV programs and one new hybrid program in 4Q, taking its cumulative EV program count to 67 across 35 customers, of which 37 are already in production and 30 remain in the launch pipeline, providing strong medium-term revenue visibility.

* Electrification momentum has strengthened materially, with strong BEV growth trends observed across Europe, India and North America in 4Q.

* The company indicated that distress among certain European competitors is beginning to translate into tangible order flow, and expects meaningful share gains in Europe in the coming years due to industry consolidation.

* Given the cost headwinds and strong growth expected from lower-margin traction motors, management has lowered its margin guidance band to 23-25% now from 24-26% earlier.

* Near-term railway growth is expected to be driven by capacity expansion, operational improvement and white-space penetration within existing brake, coupler and suspension categories. Newly developed products are expected to contribute more materially over a 3–5 year horizon.

Valuation and view

* Considering better-than-expected revenue growth in 4Q, we raise our earnings estimates by 1%/6% for FY27/FY28. The global auto demand slowdown and a slower-than-expected EV transition in key markets remain the key concerns for SONACOMS. Thus, while SONACOMS enjoys a healthy order backlog, it may see execution challenges given the expected slower EV transition. The stock at 49x/42x FY27E/FY28E factors in most positives. We reiterate our Neutral rating with a TP of INR546, valued at 38x FY28E EPS.

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041