Neutral Shree Cement Ltd for the Target Rs. 26,000 by Motilal Oswal Financial Services Ltd

Performance in line; strong volume growth

Capacity utilization improves; cost pressure a key concern

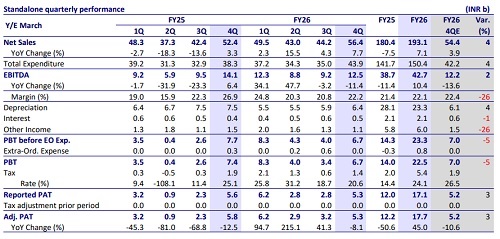

* Shree Cement’s (SRCM) 4QFY26 operating performance was in line with our estimates. EBITDA declined ~11% YoY to INR12.5b (due to cost pressure) and EBITDA/t declined ~19% YoY to INR1,161 (estimated INR1,139). OPM contracted 4.8pp YoY to ~22%. Adj. PAT declined ~8% YoY to INR5.3b (in line).

* Management indicated that cost pressures remain elevated, with near-term inflation of ~INR150–200/ton, driven by fuel, freight, and packaging costs. It is taking a price hike to offset cost increases. Structural cost-saving initiatives for renewable power, WHRS, rail logistics, and clinker optimization continue to reinforce its low-cost leadership. The RMC business is scaling gradually, with expansion to ~50–55 plants in FY27, positioning it as a long-term growth lever. Overall capacity utilization improved to ~66% in 4QFY26 from ~56% in 3QFY26, and the company remains focused on further improving capacity utilization.

* We maintained our earnings estimates for FY27/FY28E. SRCM trades fairly at 17x/14x FY27E/FY28E EV/EBITDA. We reiterate our Neutral rating with a TP of INR26,000 (based on 16x FY28E EV/EBITDA).

Volume increases ~9% YoY; EBITDA/t declines ~19% YoY to INR1,161

* Standalone revenue/EBITDA/PAT stood at INR56.4b/INR12.5b/INR5.3b (+8%/-11%/-8% YoY and +4%/+2%/+3% vs. our estimates) in 4QFY26. Sales volumes grew ~9% YoY to 10.8mt (in line). Cement realization was flat YoY (up ~2% QoQ) at INR4,732/t.

* Opex/t increased ~5% YoY (+3% vs. our estimate), led by variable/freight/ staff expenses per ton, which increased ~10%/7%/1% YoY, while other expenses/t declined ~10% YoY (benefited from positive operating leverage). OPM contracted 4.8pp YoY to ~22%, and EBITDA/t declined ~19% YoY to INR1,161. Depreciation declined 15% YoY. Other income declined 25% YoY.

* In FY26, standalone revenue/EBITDA/PAT stood at INR193.1b/INR42.7b/INR17.7b (up 7%/10%/45% YoY). OPM expanded 70bp YoY to ~22%. EBITDA/t grew ~8% YoY to INR1,174. OCF stood at INR34.9b vs. INR50.6b in FY25. Capex stood at INR14.2b vs. INR34.7b. FCF stood at INR20.7b vs INR15.9b in FY25.

Highlights from the management commentary

* It guided volume growth of 1pp ahead of industry growth. Industry cement demand growth is expected to be at ~7-7.2% in FY27, implying ~8–8.5% growth for the company. It targets to achieve ~40mt of volume in FY27.

* Fuel cost stood at ~INR1.60/kcal in 4Q and is expected to rise by ~10–12% in 1QFY27 due to geopolitical disruptions and tight global energy markets. Green power share was at 61% vs. 59%/60% in 4QFY25/3QFY26.

* Capex is pegged at INR15.0b for FY27, focused on three key areas - expansion of RMC plants, development of railway sidings, and preliminary work for the Meghalaya expansion project.

Valuation and view

* SRCM’s 4Q operating performance was in line with our estimates as higherthan-estimated realization was offset by higher-than-estimated opex/t. The company has reported strong volume growth, driven by the ramp-up of capacity utilization. While elevated costs due to higher fuel, packaging, and oil prices remain a key concern in the near term, the company is focused on rapidly expanding the RMC business, which will enhance geographical reach, optimize logistics costs, and support incremental volume growth.

* We estimate a CAGR of 9%/10%/13% in revenue/EBITDA/PAT over FY26-28. We estimate a volume CAGR of ~8% over FY26-28 (vs. muted volume CAGR over FY24-26). We estimate EBITDA/t of INR1,143/INR1,228 in FY27/FY28 vs. INR1,174 in FY26. SRCM trades at fair valuations of 17x/14x FY27E/FY28E EV/EBITDA. We reiterate our Neutral rating with a TP of INR26,000 (based on 16x FY28E EV/EBITDA).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412