Neutral Shoppers Stop Ltd For Target Rs. 370 By Motilal Oswal Financial Services Ltd

Premium push driving growth; Earnings recovery gradual

* Shoppers Stop (SHOP) delivered its strongest departmental store performance in a decade with FY26 LFL growth of 4.7%, supported by premiumization, improved footfalls, and healthy traction across non-apparel categories. Renovated stores continue to post materially higher productivity.

* Margins remained under pressure due to the high base created by one-off provision reversals in FY25. FY26 pre-IND AS EBITDA stood at INR1.4b, with margins contracting ~80bp YoY to 2.7%. However, management indicated underlying operational margins improved, aided by better mix, lower discounting, and tighter cost-control initiatives.

* Despite capex of ~INR1.2b during FY26, inventory optimization (~INR1.5b reduction) and tighter working capital management supported strong OCF (INR2.8b) and debt reduction (INR1.1b). Management reiterated its target of becoming debt-free by FY27E.

* Within INTUNE, management has shifted focus from aggressive rollout toward improving unit economics, productivity, and inventory efficiency after a slower-than-expected initial ramp-up. Targeting new venture losses to halve from ~INR0.8b in FY26 in FY27, achieving breakeven by FY28E.

* SHOP’s repositioning toward premium retail is driving improvement in productivity and customer metrics. However, medium-term growth visibility remains relatively moderate given calibrated store expansion.

* We raise our FY27/28E revenue and EBITDA estimates by 1–6%. However, continued losses in new ventures and structurally low margins in the core business are likely to keep overall profitability constrained.

* We value SHOP at 18x FY28E pre-IND AS EBITDA to arrive at our revised TP of INR370. We reiterate our Neutral rating on the stock.

Premiumization holding up growth; margins disappoint

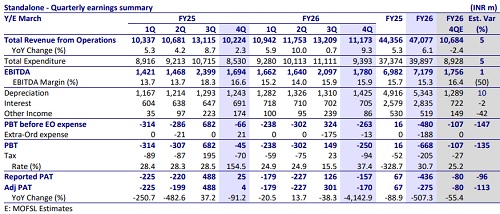

* Shoppers Stop's standalone revenue was up 9% YoY at INR11.2b (5% ahead of our est.), led by strong LFL growth in core departmental stores.

* Departmental store revenue grew 6% YoY, driven by robust 5% LFL growth. The full-year revenue surpassed INR50b with 4.7% LFL, the highest in 10 years.

* Premiumization continues to drive growth, with the premium mix growing 11% YoY (LFL 10% vs. 6%/14% in 3Q/2Q). Personnel shoppers reported INR12b in revenue, with contributions increasing 400p YoY.

* Beauty segment’s (ex-distribution) revenue declined 7% YoY, while including distribution, revenue grew 17% YoY. On a full-year basis, Beauty (including distribution) rose 17% YoY, led by a spurt in distribution revenue (+81% YoY). * Revenue from In-tune stood at INR670m (vs. INR770m QoQ, up 24% YoY) with presence expanding to 84 stores (vs. 81 QoQ). Full year up 46% YoY. ? Store additions were muted, with the store count remaining flat YoY at 295. It added a net of three departmental/INTUNE stores but closed beauty EBOs.

* The respective store count was: Departmental: 113 (4 opened, 1 closed), Beauty: 73 (7 closed), Intune: 84 (4 opened, 1 closed), and Home Stop: 12 (1 addition) for a total store count of 295.

* Gross profit inched up 2% YoY to INR4.6b (1% below our estimate) as gross margin contracted ~280bp YoY to 41.6%.

* Employee costs grew 10% YoY, while other expenses declined 4% YoY.

* EBITDA grew 5% YoY to INR1.8b (in line) with the margin at 15.9% (contracting ~65bp YoY, a 50bp miss), owing to lower gross margin.

* Pre-Ind-AS operating profit stood at INR270m (down 14% YoY), with margins at 2.2% (vs. 2.9% in 4QFY25).

* Depreciation and interest costs were up 15%/2% YoY. Other income declined 50% YoY, further hurting profitability. ? Reported loss stood at INR183m (vs. profit of INR25m YoY).

Full-year performance

* Standalone revenue grew 6% YoY to INR47b.

* Gross margin was hit, contracting 110bp to 40.2%. ? Employee costs were up 6%, while others grew 2% YoY.

* Better cost controls were partly offset by lower gross margin, leading to a 50bp dip in EBITDA margin to 15.3%; EBITDA was up 3% YoY to INR7.2b.

* Lease rentals grew 9% YoY to INR5.8b in FY26 to 11.4% of sales (up 27bp YoY).

* FY26 Pre-IND AS EBITDA stands at INR1.4b (vs. INR1.7b YoY) with margins at 2.7% vs. 3.5% in FY25.

* Depreciation grew by 9%, while finance costs declined by 11%. ? Adj. loss stood at INR275m (vs. INR67m profit in FY25).

* Core WC stood at (-)30 days (INR3.9b), down 50% YoY, owing to a dip in inventory days (down 10 days to 148). SHOP has repaid borrowings worth INR1.1b in FY26, taking the total debt to INR1.5b (on track to be debt-free by FY27).

* Despite lower profitability, WC optimization has led to a strong improvement in OCF (post-leases + interest) at INR2.7b (vs. INR247m YoY). Capex also declined 25% YoY to INR1.2b owing to a slow ramp-up in INTUNE stores, resulting in an FCFF generation of INR1.5b.

Segment performance

? The core segment reported INR12.8b revenue (4% YoY) with pre-IND AS EBITDA at INR500m (down 12% YoY) and a margin of 3.9% (down ~75bp on account of operating deleverage). ? New Ventures reported sales of INR720m (up 30% YoY), with a pre-IND AS EBITDA loss of (-) INR210m (increasing 11% YoY). ? Segment-level EBITDA included other income.

Highlights from the management commentary

* Department stores delivered 4.7% LFL growth in FY26, the highest in a decade, aided by improving customer traction, with LFL customer entry rising 4%. This marks the third consecutive quarter of positive customer entry growth, with momentum improving, supported by weddings, local travel, and resilient discretionary demand. However, inflationary pressures and potential supplychain disruptions pose near-term risks.

* Premiumization driving productivity: Premium categories and non-apparel segments such as beauty (24% YoY in FY26), watches (16%), handbags (10%), and fragrances (12%) continued to outperform, supported by higher ASPs and improved customer engagement.

* INTUNE grew 46% YoY in FY26, with store count reaching 84 across 39 cities. Management has shifted focus from aggressive expansion toward improving unit economics through inventory rationalization (~INR370m reduction), lower discounting, and better assortment. Operating KPIs and LFL trends turned positive from Feb’26 onwards and sustained into Apr’26. Expansion will remain calibrated in 1HFY27, with management targeting new venture losses to halve in FY27 (vs INR0.8b in FY26) and achieve breakeven by FY28E

Valuation and view

* SHOP’s repositioning toward premium retail is driving improvements in productivity and customer metrics. However, medium-term growth visibility remains relatively moderate given calibrated store expansion and stabilization of INTUNE, where management has shifted focus from an aggressive rollout to improving unit economics and profitability.

* We raise our FY27/28E revenue and EBITDA estimates by 1–6%. However, continued losses in new ventures and structurally low margins in the core business are likely to keep overall profitability constrained. ? We value SHOP at 18x FY28E pre-IND AS EBITDA to arrive at our revised TP of INR370. We reiterate our Neutral rating on the stock.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041