Neutral One 97 Communications Ltd for the Target Rs. 1,300 by Motilal Oswal Financial Services Ltd

Revenue growth healthy; operating leverage to improve

PIDF impact leads to EBITDA decline QoQ

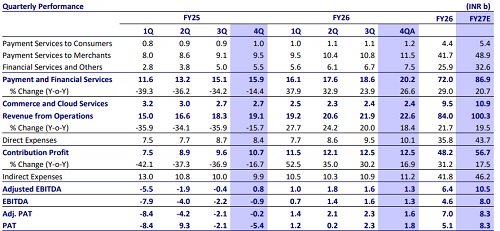

* One 97 Communications (PAYTM) reported better-than-expected revenue (up 18% YoY/3% QoQ) and largely in-line adj. PAT of INR1.6b in 4QFY26.

* Revenue grew 18% YoY/3% QoQ to INR22.64b (4% beat), aided by healthy GMV, market share gains in both consumer and merchant payments, and growth in the distribution of financial services. Financial services revenue grew 38% YoY/12% QoQ, aided by strong merchant lending partnerships.

* Net payment margin contracted 5% QoQ (1% YoY) to INR5.8b (9bp of GMV vs. 10bp in 3QFY26) amid the absence of PIDF incentive. Payment processing margin (PPM) remained above 4bp, aided by product enhancements, pricing discipline and improved credit card mix on UPI rails.

* Contribution margin declined 72bp YoY/154bp QoQ to ~55.4% (est. 55.6%), aided by better revenue growth, which was offset by an increase in direct expenses (due to higher promotional cashback and incentives).

* We increase our contribution profit assumptions by 12% for FY27/28E, led by steady revenue growth and estimate FY27E PAT at INR8.3b in FY27E and INR17.9b in FY28E. We value PAYTM at INR1,300, based on 22x FY30E EBITDA discounted to Sep’27E, translating into 7.6x Sep’27E sales. We retain our Neutral rating on the stock.

GMV growth healthy; contribution margin in line

* PAYTM reported adj. PAT of INR1.6b (broadly in line), aided by healthy GMV and steady payments and financial services revenue. GMV increased 27% YoY/5% QoQ to INR6.5t.

* Revenue grew 18% YoY/3% QoQ to INR22.64b (4% beat), led by payments and financial services (up 27% YoY/8% QoQ), while financial services revenue grew 38% YoY/12% QoQ. Subscription revenue (calc) was up 16% YoY/flat QoQ.

* Revenue from marketing services was flat QoQ at INR2.4b, while MTU rose 7% YoY/1% QoQ.

* PPM stood above 4bp, expanding from 3bp in 3QFY26. PAYTM continues to see an improvement in PPM amid higher growth of credit cards on UPI and expansion of offerings such as EMI. Net payment margin expanded 1% YoY/fell 5% QoQ to INR5.8b (9bp vs. 10bp in 3Q) amid the absence of PIDF incentive.

* While the cost was high in 4Q, management expects it to grow at a slower rate than the revenue rate, resulting in improved operating leverage.

* Direct expenses grew 20% YoY/7% QoQ, led by high promotional cashbacks and incentives. As a result, contribution profit was flat QoQ, while the contribution margin contracted 154bp QoQ to 55.4% (in line).

Highlights from the management commentary

* The company expects EBITDA margins to improve further, supported by strong operating leverage. FY27 EBITDA margins are expected to be better than FY26 levels.

* Marketing services revenue is expected to see stronger growth in FY27 compared to the muted performance in FY26.

* The company remains committed to the wallet business and is awaiting approval related to wallet operations.

* The PPBL ban doesn’t have any material impact on the broader business. Management is not keen on pursuing the NBFC license at this stage, as the company remains focused on its core strengths of distribution and technology platform development.

Valuation and view: Reiterate Neutral with a TP of INR1,300

* PAYTM reported a strong quarter, led by healthy revenue growth amid robust GMV expansion and market share gains in the payments business. The company expects revenue growth in FY27 to exceed the 22% achieved in FY26, while indirect expenses are likely to grow at a slower pace than revenue.

* Payment processing margins improved to 4bp vs. the earlier guidance of 3bp, aided by higher contributions from profitable MDR-bearing instruments, including credit cards on UPI and EMI transactions.

* Paytm continues to progress steadily toward sustainable profitability, supported by improving operating leverage, while GMV growth remained healthy and resilient.

* Contribution margin came in at 55.4%, impacted by promotional and cashbackrelated incentives; however, favourable trends in the lending business are expected to support better contribution margins going forward.

* The company has been able to absorb nearly 30-40% of PIDF-related costs and aims to offset a larger portion in the coming periods.

* We increase our contribution profit assumptions by 12% for FY27/FY28E, led by an increase in revenue, partly offset by an increase in direct expenses. We project PAT at INR8.3b in FY27E and INR17.9b in FY28E. We value PAYTM at INR1,300, based on 22x FY30E EBITDA discounted to Sep’27E, translating into 7.6x Sep’27E sales. We retain our Neutral rating on the stock.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

-96767.jpg)