Neutral Manappuram Finance Ltd for the Target Rs. 315 by Motilal Oswal Financial Services Ltd

Strong gold loan growth but NIM remains under pressure

Yields expected to now stabilize; non-gold portfolio asset quality concerns persist

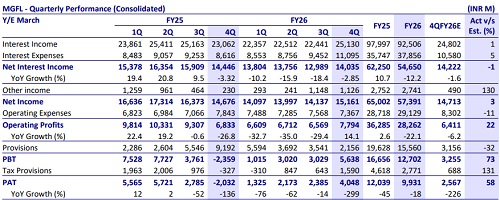

* Manappuram Finance’s (MGFL) consol. PAT improved to ~INR4.05b in 4QFY26 (PY: -INR2b; ~58% beat). FY26 PAT declined ~18% YoY to ~INR9.9b. 4Q NII declined ~3% YoY to ~INR14b (in line). Operating expenses declined 6% YoY to ~INR7.4b (11% lower than est.).

* PPoP grew ~14% YoY to ~INR7.8b (~22% beat). Consol. credit costs stood at ~INR2.2b (vs. est. of ~INR3.2b). Annualized credit costs for the quarter stood at ~1.5% (PQ: ~2.9%).

* MGFL expects to sustain growth in FY27, led by strong gold loan momentum, supported by a robust franchise, and disciplined underwriting. Regulatory easing for branch expansion is expected to help scale up distribution, and management expects to add ~500-550 gold loan branches in FY27, while partnerships and co-lending will broaden its reach beyond branch presence.

* New offerings across consumption and income-generation gold loans and affordable housing are expected to aid in portfolio diversification. With a calibrated approach in non-gold segments (MFI and VF), along with a stable operating profile, the company is well positioned for healthy AUM growth in FY27.

* Asset quality is expected to improve across MFI and VF, supported by tighter underwriting, stronger credit controls and enhanced recovery efforts. In MFI, the new book (~59% of the MFI loans) continues to replace the legacy MFI pool (~41%), with higher CE (~99.4% vs ~98.6%), driving overall portfolio improvement; the legacy book is expected to reduce to ~10% by 3QFY27. In vehicle finance, focused collection actions and digital interventions have improved bounce recoveries from ~75% to ~90%. This portfolio rebalancing and operational strengthening should translate into moderation in credit costs and gradual improvement in asset quality.

* MGFL delivered a strong performance in the gold loan segment, supported by rising gold prices, healthy demand, and a gradual shift in customer preference toward formalized financing. However, growth in the non-gold portfolio has remained subdued, primarily due to ongoing asset quality concerns, even as the VF and Asirvad MFI segments show early signs of improvement.

* The stock trades at 1.6x FY27E P/B. Over FY26-28, we estimate a CAGR of 25%/23% in gold/consolidated AUM and ~66% in consolidated PAT, with consolidated RoA/RoE of ~3%/14% in FY28. Reiterate our Neutral rating on the stock with a TP of INR315 (based on 1.5x FY28E consolidated BVPS).

Gold loans almost doubled in FY26; gold tonnage rose 7% QoQ

* Gold AUM grew ~32% QoQ and ~99% YoY to ~INR509b. Gold tonnage grew ~7% QoQ to ~63 tons.

* Within gold loans, LTV was stable QoQ at ~57%, while the average ticket size (ATS) in gold loans rose to INR128k (PQ: INR101k). Gold loan customer base grew ~3% QoQ to ~2.7m.

* Consol. Total AUM rose ~48% YoY and ~22% QoQ to ~INR638b. We expect MGFL to deliver ~23% AUM CAGR over FY26-28E, driven primarily by strong gold loan growth of ~25% CAGR during the same period.

Margins under near-term pressure, with stabilization expected ahead

* Consol. NIM (calc.) declined ~95bp QoQ to ~9.8%. Net yields on the standalone business declined ~80bp QoQ to 17.7%, while standalone CoB declined ~20bp QoQ to 8.6%, resulting in a ~60bp decline in spreads to 9.1%.

* Gold loan yields declined to ~17.3% (PQ: 18.3%) in 4QFY26. Margins are expected to remain stable going forward, with gold loan yields normalizing in the ~17.5-18% range after a sustained bout of compression. This stability will be complemented with a calibrated focus on lower-ticket, higher-yielding segments. We expect margins to stabilize going forward, with NIMs projected at ~10.1%/~10.2% for FY27E/FY28E.

Asirvad MFI shows early signs of recovery with improving collections

* Asirvad reported 4QFY26 profit of INR130m (vs. loss of INR1.6b in 3QFY26).

* Asirvad AUM (including gold loans) grew ~12% QoQ to ~INR68b, while Asirvad MFI AUM rose 4% QoQ to ~INR46.4b

* MFI GNPA declined ~10bp QoQ to 4.8%, while NNPA declined ~20bp QoQ to ~1.6%. Asirvad credit costs stood at ~INR90m (PQ: ~INR2.5b). This was aided by write-backs from mark-to-market (M2M) on the security receipts and ECL provision release.

Highlights from the management commentary

* MGFL plans to significantly expand its gold loan branch network by adding ~500- 550 branches. Regulatory changes removing prior approval requirements for branch openings are expected to facilitate faster branch expansion.

* MFI operations remain in a recovery phase, with a cautious and calibrated approach toward growth.

Valuation and view

* MGFL reported a mixed performance, with continued pressure on profitability due to NIM compression and weakness in the non-gold portfolio. Gold loan growth remained a key positive, although gold loan yields exhibited sharp compression. However, management believes that margins have likely bottomed out and guided for stability in yields in the quarters ahead. Asset quality across vehicle finance and the recovery trajectory of Asirvad MFI remain monitorable, despite initial signs of improvement.

* The stock trades at 1.6x FY27E P/B. Over FY26-28, we estimate a CAGR of 25%/23% in gold/consolidated AUM and ~66% in consolidated PAT, with consolidated RoA/RoE of ~3%/14% in FY28. Reiterate our Neutral rating on the stock with a TP of INR315 (based on 1.5x FY28E consolidated BVPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041