Neutral LTTS Ltd For Target Rs. 4,400 by Motilal Oswal Financial Services Ltd

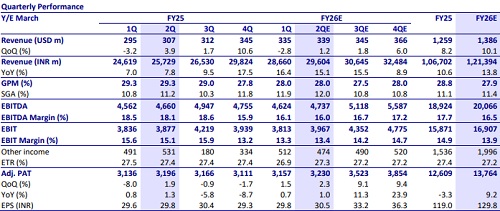

* We expect revenue to grow 1.0% QoQ CC in 2Q, as we build in gradual recovery from seasonally weak 1Q. 2H should be better than 1H, backed by deal ramp-ups.

* We expect the Sustainability vertical to lead growth, supported by deal flows and ramp-ups, while Mobility and Hi-Tech are likely to remain soft.

* We expect margins to improve marginally by ~10bp QoQ. Effective execution on margin levers, such as delivery pyramid optimization and higher offshoring, remains critical.

* We expect LTTS to retain its FY26 double-digit revenue growth guidance. Commentaries on turnaround in Mobility & deal signings will be key to track.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Financials Banking Sector Update : Reconciling banking business updates with systemic data b...