Neutral L&T Technology Ltd for the Target Rs. 3,400 by Motilal Oswal Financial Services Ltd

Reset underway Portfolio exits and divestment weigh on growth

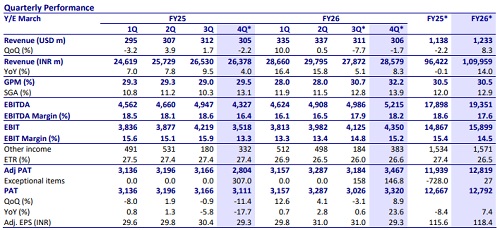

* L&T Technology’s (LTTS) 4QFY26 revenue declined 1.1% QoQ in CC terms. The company has divested its SWC business, which has been classified as a discontinued operation, effective 4QFY26. Accordingly, reported financials are not directly comparable with estimates. For FY26, revenue stood at USD1.2b, up 7.7% YoY CC. Sustainability segment grew 1.6% QoQ, while Tech declined 6.3% QoQ. Mobility was flat QoQ.

* EBIT margin stood at 15.2%, up 40bp QoQ. Adj. PAT was up 8.9% QoQ/1.4% YoY at INR3.5b. For FY26, adj. PAT stood at INR13b, up 7.4% YoY.

* For FY26, revenue/EBIT/adj. PAT grew 14.0%/6.9%/7.4% YoY in INR terms. In 1QFY27, we expect revenue/EBIT/adj. PAT to grow 1.9%/18.8%/13.4% YoY. Free cash flow stood at 100% of net profit in FY26 (vs. 109% in FY25). FY26 RoE came in at 20.3% (vs. 22.1%/25.3%/25.6% in FY25/FY24/FY23). We reiterate our Neutral rating on the stock with a TP of INR3,400, implying a 4% potential downside.

Our view: Building blocks in place but consistency still evolving

* Soft exit; divestment of SWC impacts reported numbers: Revenue declined 1.1% QoQ CC in 4Q to USD306m, while FY26 growth came in at 7.7% YoY CC. 4Q was impacted by portfolio exits and SWC divestment, leading to a weaker exit. With most of the cleanup behind, management expects a more stable base from 1QFY27. Given the relatively weak FY26 exit and still uneven revenue visibility, we now build in organic revenue growth of 2.0% and overall revenue growth of 7% YoY in USD in FY27.

* Sustainability steady; Mobility improving; Hi-tech reset underway: Sustainability grew 1.6% QoQ and continues to anchor performance. Mobility is showing early signs of recovery, supported by deal wins, though growth is yet to sustain. Tech declined 6.3% QoQ due to deliberate exits, but margin improvement indicates better quality of business. Management expects all segments to return to sequential growth from 1QFY27; we see improvement, but with some volatility in the near term.

* Deal wins healthy; conversion remains the key monitorable: Large deal momentum remains healthy, with ~USD200m TCV for the sixth straight quarter and FY26 TCV at USD855m (+40% YoY). This provides visibility on medium-term growth. That said, recent quarters indicate slower ramp-ups, and we would watch execution of large deals for a more consistent growth pickup.

* Margins improving; trajectory to mid-16% guidance by 4QFY27 remains key to watch: EBIT margin improved 40bp QoQ to 15.2% in 4Q4, with FY26 margin at 14.5%. Management has guided for 16-17% margins over the medium term. We believe margin expansion will be driven by better segment mix (higher Sustainability), benefits from portfolio rationalization, and AI-led efficiencies, though gains are likely to be incremental. We expect margin of 15.2%/15.8% in FY27/FY28

* The Lakshya 31 plan targets 13-15% growth with 16-17% margins over five years, supported by themes like AI, data center capex, and re-industrialization. While the direction remains positive, near-term growth consistency is still evolving. We maintain a neutral stance, awaiting stronger deal conversion and more stable sequential growth before turning constructive.

Valuation and revisions to our estimates

* We build in a USD revenue CAGR of ~9.0% over FY26-28E, factoring in a weak FY26 exit and a gradual improvement thereafter. For FY27, we estimate ~7% YoY USD growth, as the impact of portfolio exits and SWC divestment fades and the base normalizes. Sustainability should continue to provide stability, while Mobility recovery is likely to be gradual and Tech may remain volatile in the near term.

* We expect EBIT margins to improve to ~15.8% by FY28E, led by better mix and execution. We maintain our Neutral rating with a TP of INR3,400, based on 23x FY28E EPS.

Lakshya plan targets 13-15% growth over next five years with 16-17% EBIT margins; deal TCV healthy

* USD revenue declined 1.1% QoQ CC to USD306m. For FY26, revenue stood at USD1.2b, up 7.7% YoY CC.

* The company has divested its SWC business, which has been classified as a discontinued operation, effective 4QFY26; accordingly, reported financials are not directly comparable with estimates.

* LTTS aims to deliver 13-15% CAGR over the next five years, with EBIT margins in the range of 16-17% under the five-year Lakshya 31 Plan.

* Sustainability grew 1.6% QoQ, while Tech was down 6.3% QoQ. ? EBIT margin stood at 15.2%, up 40bp QoQ. For FY26, adj. EBIT margin stood at 14.5% vs. 15.4% in FY25.

* Adj. PAT was up 8.9% QoQ/1.4% YoY at INR3.5b. For full year, adj. PAT stood at INR13b, up 7.4% YoY.

* The employee count was up 2.2% QoQ at 23,830. Attrition was down 10bp QoQ at 14.7%.

* Large deal momentum in 4Q – delivering an average TCV of USD200m for the sixth consecutive quarter.

* Deal signings: Large deal TCV touched a record high of USD855m, up 40% YoY. The board approved the final dividend of INR40/share.

Key highlights from the management commentary

* Management remains cautiously optimistic on the near-term demand environment; CY26 macro improvement is supporting the deal pipeline conversion across all three segments.

* Broad-based demand recovery visible: Mobility stabilizing, Sustainability maintaining double-digit momentum, and Tech segment bottoming out postportfolio rationalization.

* Sequential revenue moderation in 4Q was partly attributable to USD19m in annualized revenue exit from low-margin geographies (Europe, Middle East, select US tech accounts) and the SWC divestment; management confirms the base is clean 1QFY27 onward.

* First USD50m+ trailing-12-month account formally reported in the Sustainability segment; management views scaling account sizes as a key strategic priority under Lakshya 31.

Management is confident that all three Tech sub-segments (MedTech, Media/Tech, Software & Platforms) will return to sequential growth from 1QFY27.

* Wage hikes for all employees globally administered in 4QFY26 (100bp impact on margins); fully baked into the margin guidance trajectory.

* AgenticIQ platform launched - an enterprise-ready agentic AI platform for orchestration and deployment of AI agents across engineering lifecycles; positions LTTS as a platform-led solution provider, not just a point-tool vendor.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412