Neutral JSW Cement Ltd For Target Rs.130 by Motilal Oswal Financial Services Ltd

Multi-region capacity build-out gains momentum

Scaling capacity; strengthening distribution & brand recall

* JSW Cement (JSWC) is intensifying its North India focus through planned kiln additions and rapid network expansion across ~55 districts with ~900 dealers, aimed at strengthening market penetration and improving logistics efficiency. The company is on an aggressive capacity ramp-up path, targeting ~60mtpa over the next 5–6 years. Meanwhile, the company’s ongoing expansion plans across the north, west, and south is progressing as planned. Additionally, planned expansions in central India, including assets in Madhya Pradesh and Uttar Pradesh, are likely to enhance its regional footprint and support long-term growth.

* The company is scaling brand visibility through influencer-led engagement, targeting ~17,000 contractors and engineers, alongside strong on-ground initiatives to enhance retail presence. Simultaneously, it is strengthening service levels via depot expansion to ensure better product availability and faster delivery. Its dealer-centric strategy emphasizes transparency and predictable incentives, supporting dealer planning, liquidity, and long-term relationships. Operationally, the focus remains on cost-efficiency, supply chain, and product quality.

* We estimate a CAGR of 20%/21%/11% in revenue/EBITDA/PAT over FY26- 28. We estimate a volume CAGR of ~18%. EBITDA/t is estimated at INR839/ INR903 in FY27/FY28 vs. INR846 in FY26E. At CMP, the stock is trading fairly at 17x/14x FY27E/FY28E EV/EBITDA. We value JSWC at 13x FY28E EV/EBITDA to arrive at our TP of INR130. Reiterate Neutral.

Strategic capex plans underway; long-term capacity target of 60mtpa

* JSWC is strategically focusing on North India, with plans to establish four kilns (clinker production line) over the next few years. The company’s increasing presence across ~55 districts, backed by the appointment of ~900 dealers, reflects a sharp push to deepen market penetration in the region. This scale-up is expected to improve logistics efficiency, reduce lead distances, and strengthen its competitive positioning against established regional players.

* The company is aggressively scaling up its capacity with a long-term target of reaching ~60mtpa over the next 5–6 years, positioning itself among the topfive players in the Indian cement industry. Currently, it is expanding capacity through: 1) 3.5mtpa integrated cement plant at Nagaur, Rajasthan (3.3mtpa/2.5mtpa clinker/cement capacities commissioned in Mar’26, while 1.0mtpa grinding capacity under construction); and 2) ~2.75mtpa grinding unit in Punjab (likely to be commissioned in Mar’27).

* Additionally, the upcoming Vijayanagar and Dolvi expansions are expected to be commissioned over the next ~1.5-2.0 years in a phased manner. Management indicates that these projects are low capex-intensive and are expected to drive superior capital efficiency and return ratios. The company also has expansion plans for central India (part of its long-term expansion strategy), with an integrated plant in Madhya Pradesh and a split grinding unit in Uttar Pradesh, catering to key markets of central India and Delhi.

Brand push and dealer engagement to strengthen market positioning

* The company is investing heavily in brand visibility and influencer-driven demand creation. It has identified ~17,000 decision-making influencers (including contractors and engineers) and is actively engaging with them to drive product adoption. On-ground branding efforts include ~155 hoardings and painting of ~500 dealer shops (with more in progress), significantly improving retail visibility. JSWC is also working on enhancing service levels through the development of depots, ensuring better availability and faster delivery—critical factors in driving dealer loyalty and end-user satisfaction. Its positioning as ‘the world’s greenest cement company’ further strengthens its brand narrative, especially as sustainability gains importance in procurement decisions.

* JSWC follows a dealer-centric approach with a strong emphasis on transparency and return on investment. The company has introduced a structured and predictable incentive framework—schemes and incentives are announced at the beginning of the year, enabling better planning for dealers. Pricing and discount mechanisms are also streamlined, with rate revisions typically occurring twice, cash discounts offered thrice, and spurt discounts disbursed within 10 days of scheme closure. Retail-level incentives are settled within one month of quarterend, ensuring liquidity support for channel partners. Additional engagement initiatives, such as annual dealer tours and performance-linked rewards (e.g., gifts for dealers lifting 100 tons monthly throughout the year), further strengthen relationships and drive volume growth.

* The company continues to focus on product quality, service reliability, and cost efficiency. Its emphasis on low-capex expansion, efficient plant configurations, and strong supply chain infrastructure supports better margins and return ratios. The company’s push for dealer exclusivity in certain markets is also likely to improve channel stickiness and reduce competitive intensity at the retail level. With a combination of aggressive capacity expansion, strong dealer engagement, and a differentiated sustainability-led positioning, it is steadily building a scalable and competitive business model that can deliver consistent growth over the medium to long term.

Valuation and view

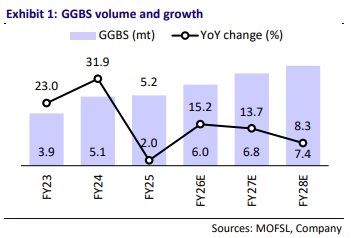

* We estimate a CAGR of ~20%/21%/11% in revenue/EBITDA/Adj. PAT over FY26- 28E, driven by higher sales volume (~18% CAGR). EBITDA/t is estimated to be INR839/INR903 in FY27/FY28 vs. INR846 in FY26E. The company’s GGBS profitability remains higher, given the cost advantage and stable realization.

* Cumulative OCF is expected to increase to INR34.0b during FY26-28 vs. INR28.0b over FY23-25, driven by improvement in profitability. Cumulative capex over FY26-28E should be higher at INR56.0b (given the aggressive capacity expansion plan) vs. INR37.2b over FY23-25. We estimate JSWC’s cumulative net cash outflow to stand at INR22.0b over FY26-28 vs. INR9.2b over FY23-25.

* Net debt is estimated to increase to INR60.5b in FY28E vs. INR43.6b as of FY26E. Net debt-to-EBITDA ratio is estimated at similar levels of 3.5x by FY28E. We value JSWC at 13x FY28E EV/EBITDA to arrive at our revised TP of INR130. Reiterate Neutral.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)